Defined Contribution or Defined Benefit and how to get the best outcome

Workplace pensions are one of the most powerful, and often misunderstood parts of financial planning in the UK. They benefit from employer contributions, tax relief, and long time horizons, yet many people treat them as background noise or least favorable option rather than a cornerstone of long-term wealth.

In this guide, we’ll break down the main types of workplace pension, explain how each works, weigh up the advantages and disadvantages, clarify the minimum your employer has to do, and explain what you should actually do to get the best possible outcome.

Quite often, when people think about retirement, they imagine a fixed income for life, “getting their pension” in the traditional sense. For a long time, that usually meant a Defined Benefit pension or buying an annuity: a predictable, guaranteed payment that turned work into retirement income automatically. This all changed with the introduction of mainstream Defined Contribution occupational pensions, stakeholder pensions, personal pensions & people contracting out of the state second pension. This process was all given a nudge with the introduction of the various updates to the Pensions Act and Pensions Freedom in 2015.

Your pension is no longer something you are given, it is something you can design.

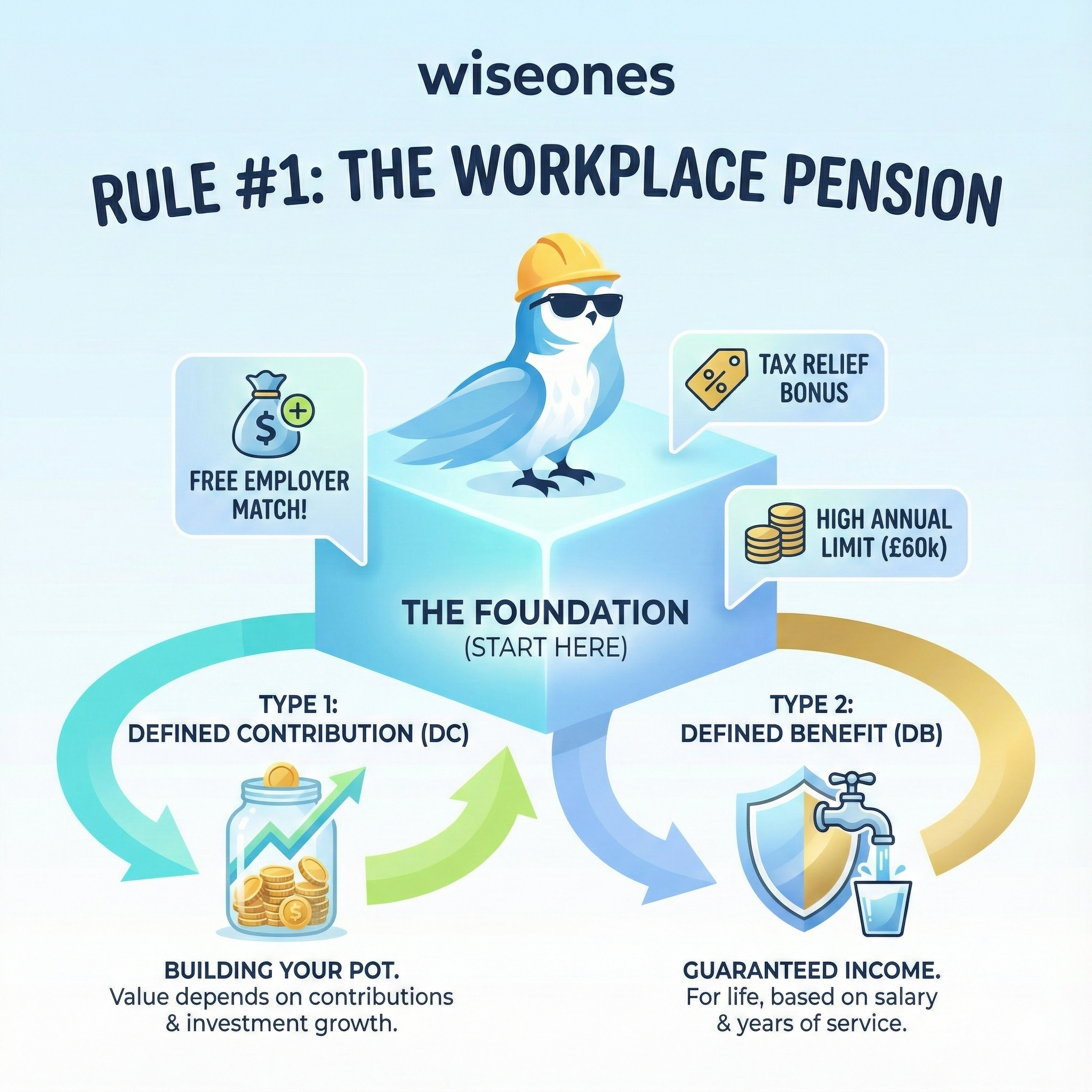

Defined Contribution (DC) Schemes

A pot of money that is in your name that you invest

Money goes in from you, your employer and tax relief

This pot of money is invested and what you get out of it depends on how much is contributed, what it is invested in and how long it is invested for.

This is the default for most private sector workers and auto-enrolment schemes.

Pro

Flexibility in how to take money out of the pension funds

Control what you are invested in

They are your funds and not tied to an employer

Con

The risk is with what you choose to invest in

Requires active management and decision making through retirement

No guaranteed income unless you purchase an annuity

At risk of poor advice

Defined Benefit (DB) Schemes

Paid out at retirement based on how many years you have worked

This is either an amount invested on your behalf and the pension scheme provider will pay out a guaranteed income for life calculated using a formula set out in the scheme rules. The investment risk sits with the scheme.

This is the default for most public sector workers, with some being unfunded (NHS, Teachers, Police) and some funded (Local Government). It was also for some old workplace pension schemes, probably the most famous of which was BHS pension scheme which had to be bailed out

Pro

No investment risk

Guaranteed payment on retirement

Generally very tax efficient

Con

No flexibility with how to take money out of the pension

They are tied to the employer

May not include spousal benefits

Not able to pass on to beneficiaries

What your employer has to do?

Since 2014 all eligible workers must be enrolled into a workplace pension scheme, that’s anyone over the age of 22 and earning over £10,000 a year. Your employer must make sure there is at least 8% of qualifying earnings with at least 3% coming from your employer directly.

What you should do?

The minimum you should do is invest to get your employer contribution into your pension, if your employer offers matching to a higher percentage then it’s often worthwhile to do that, especially where they offer generous contributions. This is extra pay that you are missing out on otherwise. Check what you are invested in, check your nominated retirement date and importantly check who you have as your beneficiary.