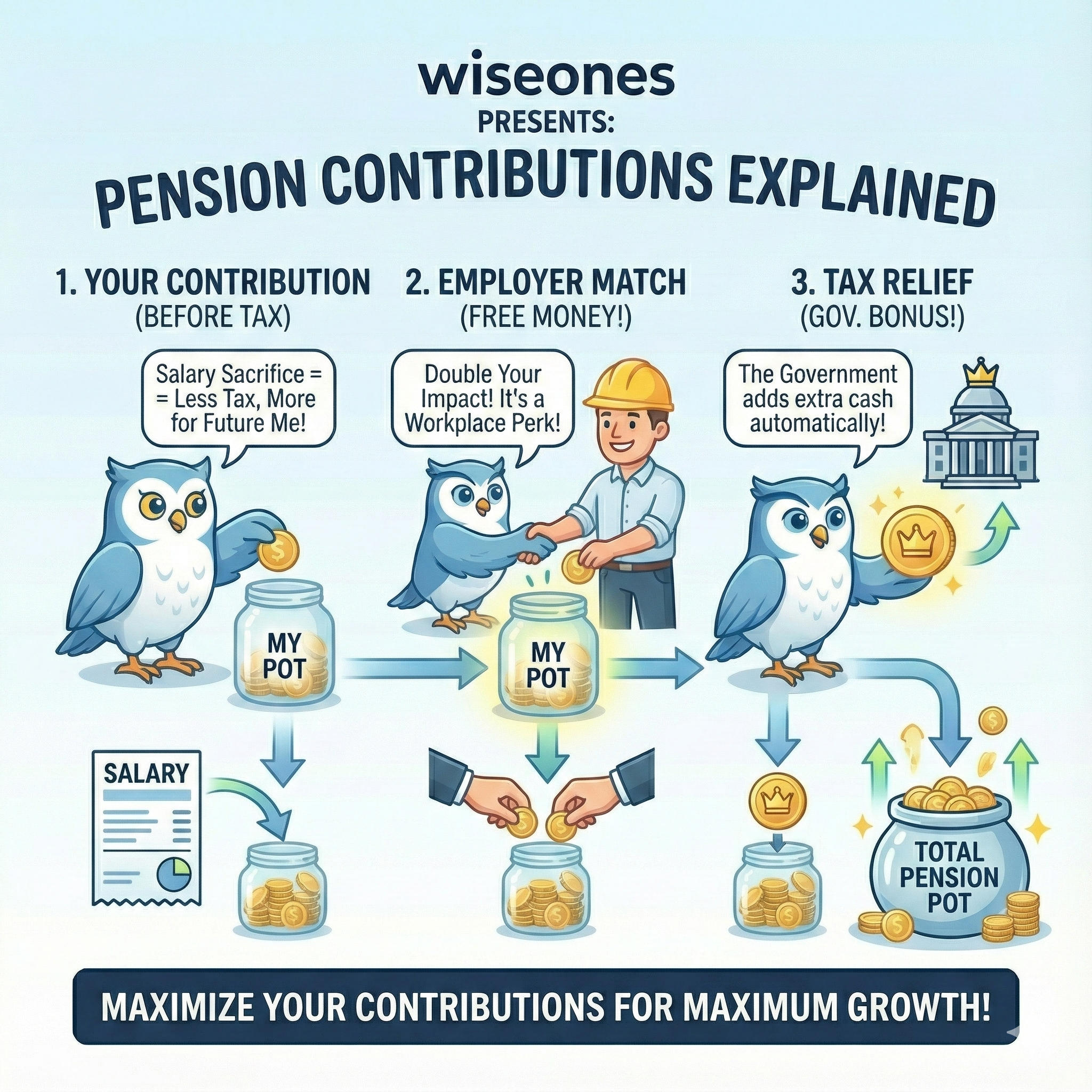

Pensions are often sold as simple: you pay some money in, your employer adds a bit, the government gives tax relief, and it grows over time.

The reality is more complicated. Not because pensions are deliberately obscure, but because how contributions are calculated and how tax relief is applied depends on the structure of the scheme. Two people paying “the same percentage” can end up with very different amounts going into their pension.

Understanding the basics of how contributions work, and checking that yours are being applied correctly, can make a meaningful difference over a working lifetime.

How Workplace Pension Contributions Work

When you contribute to a workplace pension, the first thing to understand is how the contribution is taken from your pay. Most pension providers explain this using three broad methods: Relief at Source, Net Pay, and Salary Sacrifice.

Relief at Source: The Top-Up You Don’t See

With Relief at Source, your pension contribution is taken from your take-home pay, after tax has already been deducted. Your pension provider then reclaims basic-rate tax relief from HMRC and adds it to your pension.

So if £80 leaves your payslip, £100 ends up invested.

This is how most personal pensions and many workplace schemes operate. Providers like Nest and Vanguard describe it as automatic tax relief, and at basic-rate level that’s true.

However, if you pay higher-rate or additional-rate tax, the extra relief isn’t automatic. You have to actively reclaim it, usually through Self Assessment or a tax code adjustment. Many people never do, which means they quietly miss out on tax relief they’re entitled to.

Relief at Source does have one important advantage: if you earn below the personal allowance, you still receive tax relief. That makes it particularly valuable for lower earners.

Net Pay: Relief Through Payroll

Under a Net Pay arrangement, pension contributions are taken before income tax is calculated. The tax relief happens instantly through payroll, so higher-rate taxpayers automatically get the correct relief without needing to claim anything back.

For many people, this is efficient and straightforward. This does mean that you are still paying National Insurance contributions out before making your pension contribution.

Salary Sacrifice: Changing the Question Entirely

Salary sacrifice or salary exchange works differently again. Instead of you paying a pension contribution, you agree to give up part of your salary and your employer pays that amount into your pension instead.

From HMRC’s point of view, that salary never existed.

This means no income tax and no National Insurance are paid on the sacrificed amount. Employers also save National Insurance, and many share part of that saving by increasing the pension contribution.

Most major pension providers describe salary sacrifice as the most tax-efficient way to save into a workplace pension when it’s implemented properly.

It isn’t without considerations. Salary sacrifice can affect mortgage applications, life cover, or statutory benefits if schemes aren’t set up carefully, and pay cannot fall below the National Minimum Wage. But when done well, it is hard to beat.

Qualifying (or Banded) Earnings: The Part People Miss

Even when people understand tax relief, there’s another layer that often causes confusion: what your contributions are actually calculated on.

Some automatic-enrolment workplace pensions use qualifying earnings, sometimes referred to as banded earnings.

This means contributions are not calculated on your full salary. Instead, they are based only on earnings between a lower and upper threshold set by the government.

Many employees understandably assume that a stated contribution rate applies to everything they earn.

It doesn’t.

So when you see an “8% total contribution”, that is often 8% of qualifying earnings, not 8% of your full pay. The difference can be significant, especially at lower and middle income levels.

This doesn’t mean your employer is underpaying or that the scheme is wrong — it means it’s operating exactly as the rules allow. But it does mean you may be saving less than you think.

I’ll cover qualifying earnings in full detail separately, but for now the important point is simple: percentages don’t tell the whole story.

Checking Your Contributions Are Right (And Actually Paid)

Pension providers consistently encourage people to check their contributions — not because errors are common, but because changes don’t always trigger automatic reviews.

It’s worth checking:

That contributions are deducted every time you’re paid

That they reflect your current salary, not an old one

That increases in pay result in higher pension contributions

That employer contributions are being paid promptly, not late

Even small underpayments, repeated over years, can compound into a meaningful shortfall at retirement.

Don’t Miss Employer Matching

One of the most common issues providers highlight is people missing out on employer matching.

Many employers will contribute more than the statutory minimum, but only if the employee contributes enough themselves. If you’re paying the minimum and your employer would match a higher rate, you are effectively declining part of your pay.

From a value perspective, employer matching is some of the best money you will ever receive. It’s worth making sure you’re getting all of it.

Personal Pensions, SIPPs, and Employer Contributions

Outside the workplace, most personal pensions and SIPPs use Relief at Source. You pay a contribution, your provider adds basic-rate tax relief, and higher-rate relief must be reclaimed.

Employer contributions work differently. They are paid directly by the employer, don’t count as income, and are usually an allowable business expense. For company directors in particular, employer pension contributions can be more tax-efficient than taking salary or dividends.

All contributions — personal and employer — count toward the Annual Allowance, which is currently £60,000 per tax year, with carry forward available for unused allowances from the previous three years. Higher earners also need to be aware of the tapered Annual Allowance above £200,000 salary, which can reduce this significantly.

The Bigger Picture

Pensions reward consistency, but they also reward attention.

Understanding how your contributions are taken, what they’re calculated on, and whether increases in pay translate into increases in pension funding can make a bigger difference than many of the decisions people spend time worrying about.

Most people don’t need to become pension experts. But checking that your scheme is working as you think it is — and that you’re not quietly missing out on tax relief or employer contributions — is time very well spent.