For anyone who remembers Working Lunch, there was a time when talking about shares, markets, and ownership felt normal. Investing wasn’t niche, elitist, or intimidating; it was simply what adults did with long-term money.

Today, that mindset has been flipped on its head.

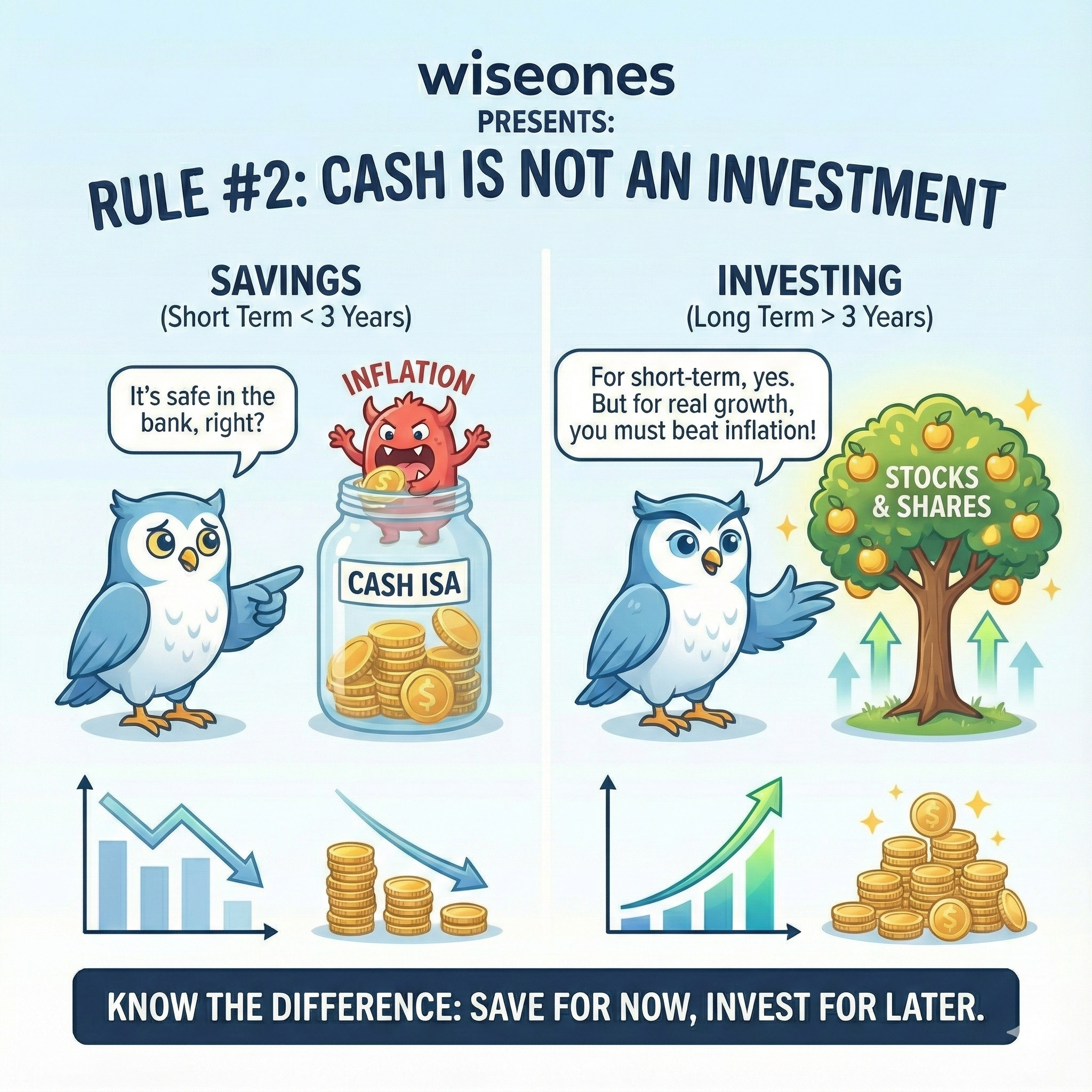

In the modern UK financial narrative, people are encouraged to start with a Cash ISA, and only later, if they become “brave enough”, move into investing. That framing is fundamentally wrong.

The starting point for any money not needed in the next few years should be a Stocks & Shares ISA.

Cash should be the side pocket, not the foundation.

Cash feels safe – but safety can be an illusion

Cash ISAs and savings accounts feel comforting. The balance never goes down. There’s no volatility, no scary headlines, no emotional discomfort.

But this sense of safety is misleading.

Inflation steadily erodes purchasing power. Even at modest levels, inflation compounds against you every single year. If real inflation averages 3–4% and your cash ISA pays something similar (or less), your real return is negative.

You still see the same number, but it buys less life, less freedom, and less security.

Cash doesn’t fail dramatically.

It fails invisibly.

A Cash ISA is a saving not an investment

This distinction is critical.

A Cash ISA is not an investment. It is a short-term savings tool.

Cash has a purpose:

Emergency funds

Short-term spending needs

Temporary holding money

What it is not designed for is medium-term growth.

A Stocks & Shares ISA, on the other hand, is an investment wrapper designed specifically to allow long-term capital growth, free of income tax and capital gains tax.

If your goal is to grow wealth over time, this should be where you begin after your workplace pension.

Cash should carry a higher risk rating

Here’s where the system gets it wrong.

Cash is labelled “low risk”.

Investing in funds, shares, bonds, etc is labelled “high risk”.

This is backwards way to look at

If you are not investing, the value of your cash is guaranteed to erode over time due to inflation. That is not a possibility, it is an almost certainty.

That makes long-term cash holding a known, unavoidable loss.

Investing, by contrast, involves short-term uncertainty but long-term probability. Over meaningful time horizons, investing has historically reduced risk by preserving and growing purchasing power.

Yet regulation, risk warnings, and public messaging still treat cash as “safe”.

This is not consumer protection, it is consumer mis-education.

Why the media obsesses over Cash ISAs

So why do financial journalists and commentators constantly focus on cash ISAs?

Partly because they can’t talk about investing — or don’t truly understand it.

Explaining investing requires nuance:

Risk over time, not day-to-day volatility

Compounding

Probability instead of certainty

Ownership instead of reassurance

It’s easier to write “best savings rate” articles than to explain how wealth is actually built.

I used to give Martin Lewis stick for this, but the reality is structural. The Financial Conduct Authority and media compliance culture discourage meaningful investment discussion in favour of “safe” messaging.

The result? A population encouraged to accept guaranteed long-term loss.

Avoiding volatility guarantees stagnation

The great irony is this:

People fear markets going down in the short term, yet willingly accept a strategy where their money loses value every single year.

Markets fluctuate.

Inflation erodes relentlessly.

If your time horizon is longer than three years, cash should be a temporary holding place, not a destination. A Stocks & Shares ISA should be the default home for long-term money for most people.

The UK doesn’t need more savers, it needs more investors

If the UK is to thrive, we need a cultural shift.

We don’t need a nation obsessed with hoarding cash.

We need a nation that understands ownership.

Ownership of companies.

Ownership of innovation.

Ownership of economic growth.

When people invest, they don’t just build personal wealth they help drive the economy itself.

The disappearance of Working Lunch symbolised the retreat of everyday investment conversation from public life. That conversation needs to come back.

Bring back investing into everyday life

Investing shouldn’t be taboo or intimidating.

It should be talked about:

With workmates over lunch

In schools

At sports clubs

And most importantly in the pub

Not speculation or hype but long-term thinking, compounding, and ownership.

UK personal wealth will flourish when people stop thinking like savers and start thinking like investors.

Stocks & Shares ISA is your starting point

Cash has a role in the short term, but longer term it is corrosive.

If your money won’t be needed for years, leaving it in cash is likely the highest-risk decision you can make, because it guarantees a loss of purchasing power.

The starting point should be a Stocks & Shares ISA.

Cash should sit on the sidelines.

It’s time to stop pretending Cash ISAs are investments and the best rates are discussed, instead build a culture where investing is normal, understood, and encouraged.

I loved watching Working Lunch – I will would vote for it coming back!