It’s all about the value for money

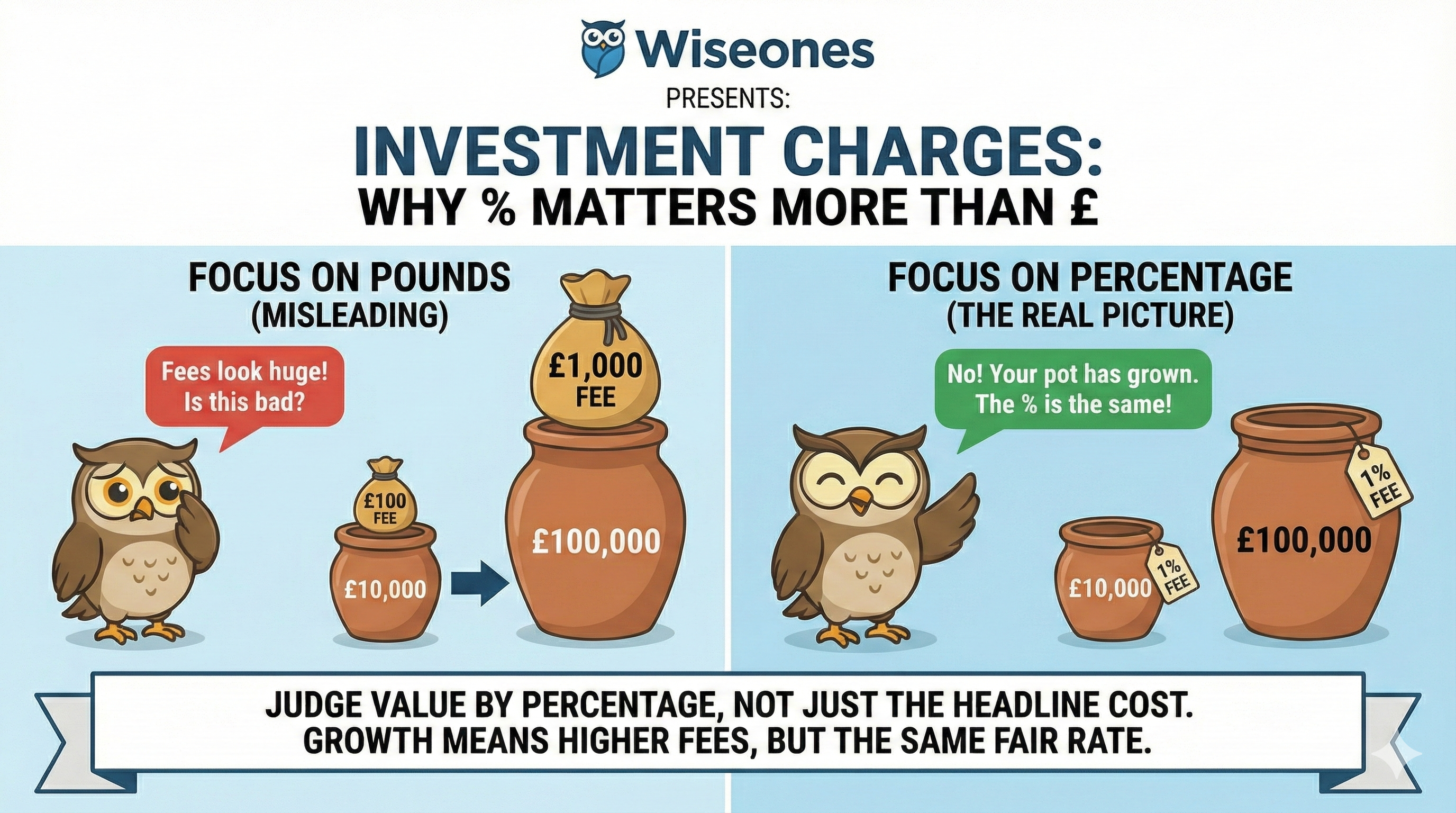

When looking at investment charges, it’s natural to focus on the pound amount being paid. As portfolios grow, fees can start to look large, sometimes uncomfortably so. But this can be misleading.

The most important figure to understand is not the cash amount, but the percentage being charged.

If the percentage remains suitable and fair, a higher pound figure often simply reflects that your investments have grown. In other words, rising fees can be a sign of progress, not a problem, provided the charges remain appropriate and deliver value.

This is why good financial guidance focuses on value for money, not just headline cost.

Financial Adviser Charges

Initial Adviser Charges or Ad-hoc charges

Initial charges cover the work required to put a suitable plan in place, including:

Understanding your objectives and circumstances

Assessing risk and capacity for loss

Research, recommendations, and suitability reports

Structuring and implementing investments

These charges are agreed upfront and are designed to ensure advice is appropriate, documented, and defensible. These could also be a one off charge if you are not having ongoing advice.

Ongoing Adviser Charges

Ongoing adviser charges cover continued support and oversight, such as:

Regular reviews and rebalancing

Keeping advice suitable as your life changes

Ongoing planning, guidance, and accountability

Crucially, ongoing charges also reflect the adviser’s long-term professional responsibility to the client.

Why Charges Exist at All

Charges are an inherent part of investing. Whether you invest directly or with professional support, costs exist for administration, management, regulation, and protection.

The aim is not to eliminate charges but to ensure they are:

Transparent

Proportionate

Suitable for your needs

Delivering clear value

Left unchecked, charges can erode returns over time. Managed properly, they support better decisions, stronger governance, and long-term outcomes.

Provider and Platform Charges (Including AMC)

Most investments are held with a provider or platform, particularly pensions and ISAs.

The Annual Management Charge (AMC) is the charge taken by the provider or platform. It typically covers:

Administration and record keeping

Governance and regulatory responsibilities

Reporting and online access

In some arrangements, the AMC may include access to a default fund or a limited range of funds. However, this is not always the case, and many funds sit outside the AMC and carry their own charges.

Modern platforms may show this as a separate platform fee, but the purpose is the same: running and maintaining the investment wrapper.

Fund Charges: The Cost of Managing the Investment

Fund charges are separate from platform or AMC costs and relate to managing the underlying investments.

They pay for:

Investment decision-making

Asset selection and risk management

Research and trading within the fund

These charges are usually shown as the Ongoing Charges Figure (OCF) and are deducted within the fund itself.

Actively managed funds generally cost more than passive funds, but higher charges do not guarantee better performance. Suitability and value are what matter.

Discretionary Fund Manager (DFM) Charges

Some investors use a Discretionary Fund Manager (DFM) to manage their portfolio on a day-to-day basis.

DFM charges cover:

Portfolio construction and asset allocation

Ongoing monitoring and rebalancing

Risk management and tactical changes

These charges sit on top of platform and fund costs and should only apply where the service adds clear value.

Dealing Charges

Dealing charges may apply when investments are bought or sold, for example when switching funds or rebalancing a portfolio. These may be charged per transaction or built into platform pricing.

Frequent trading increases costs, which is why long-term, disciplined investing is usually more efficient.

FX (Foreign Exchange) Charges

When investing in overseas assets, foreign exchange charges can apply when money is converted into or out of another currency.

These charges are often small, but repeated conversions can have a cumulative impact on returns.

Bid–Offer Spread: A Hidden Cost

The bid–offer spread is the difference between the price you buy an investment at and the price you could sell it for immediately.

Assets that usually have a spread:

Shares, ETFs, investment trusts, and directly traded bonds.Assets that generally don’t:

Open-ended funds (OEICs and unit trusts) and most workplace pension default funds, which are priced once per day at a single price.

Spreads are a normal part of markets, but they are still a real cost — particularly for less liquid or frequently traded assets.

Why Adviser Charges Are About More Than Time

Many people assume adviser fees are simply payment for time spent. In reality, they also cover:

Regulatory compliance and oversight

Professional indemnity insurance

Record keeping and audit trails

The client’s right to return many years later if advice is ever questioned

This protection exists for the client’s benefit and is a fundamental part of regulated financial advice under the FCA framework.

Consumer Duty and Value for Money

Under Consumer Duty, firms must ensure charges represent fair value, considering:

The benefits received

The quality of service

The ongoing support and protection provided

A charge can look expensive in cash terms but still represent good value if the percentage is appropriate and the service delivered remains suitable.

The Wiseones View

At Wiseones, we believe charges are not the enemy. Poorly understood or unsuitable charges are.

The right focus is on:

Percentages, not headlines

Value, not just cost

Long-term suitability, not short-term optics

When charges are transparent, fair, and aligned to real outcomes, they support better decisions and greater peace of mind. This is exactly what good financial advice and management should deliver.