(and one way to leave it in the nest)

Think of your pension pot as a cooked egg.

Yolk = your 25% tax-free cash

White = the other 75%, taxed as income when you take it out

Every defined contribution pension works like this. Workplace pensions, SIPPs, personal pensions, the lot. What changes is how you crack it and when you eat it.

And before we start cracking: from 6 April 2028, the minimum age to access most pensions rises from 55 to 57 (with some protected exceptions).

Right. Here are your options, in plain English, with the tax tripwires highlighted where they actually bite.

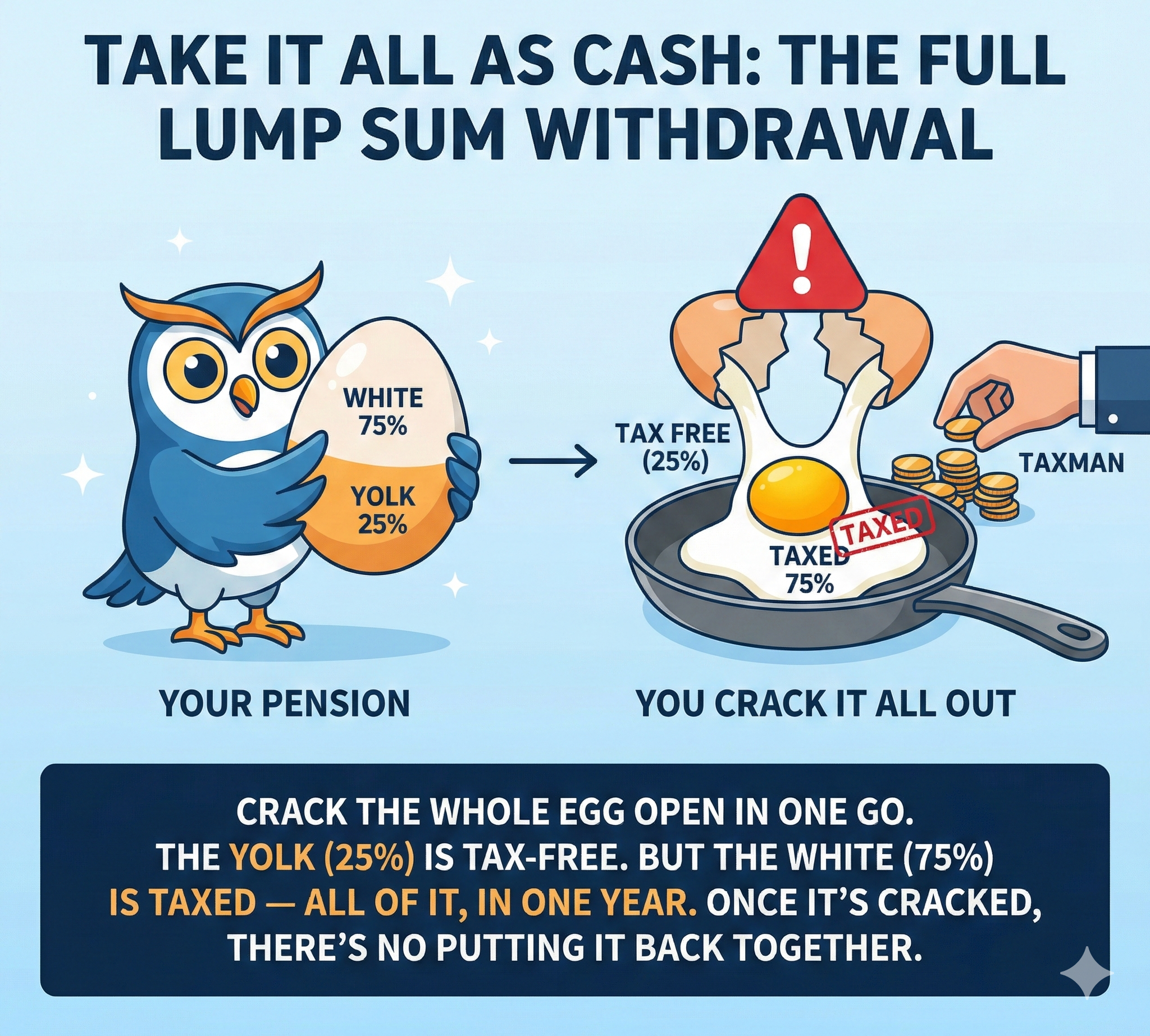

Option 1: Crack the whole egg in one go

Take it all as cash: The full lump sum withdrawal

This is the nuclear option. You take the entire egg, yolk and white, in one tax year.

25% yolk lands tax-free

75% white gets added to your income and taxed at your marginal rate (often dragging you into higher or additional rate)

Then the egg is gone:

no more tax-sheltered growth

no more pension wrapper advantages

just cash sitting in an account, quietly losing purchasing power

MPAA warning (yes, this one can trigger it)

If your “take it all” payment includes taxable white (it will), you’ve taken taxable pension income, which means you can trigger the Money Purchase Annual Allowance (MPAA). That can cut what you’re allowed to contribute to money-purchase pensions in future to £10,000 a year (instead of the standard annual allowance).

Who it’s for: usually almost nobody with a meaningful pot. The trap: emergency tax codes can mean you overpay tax up front and have to reclaim it later.

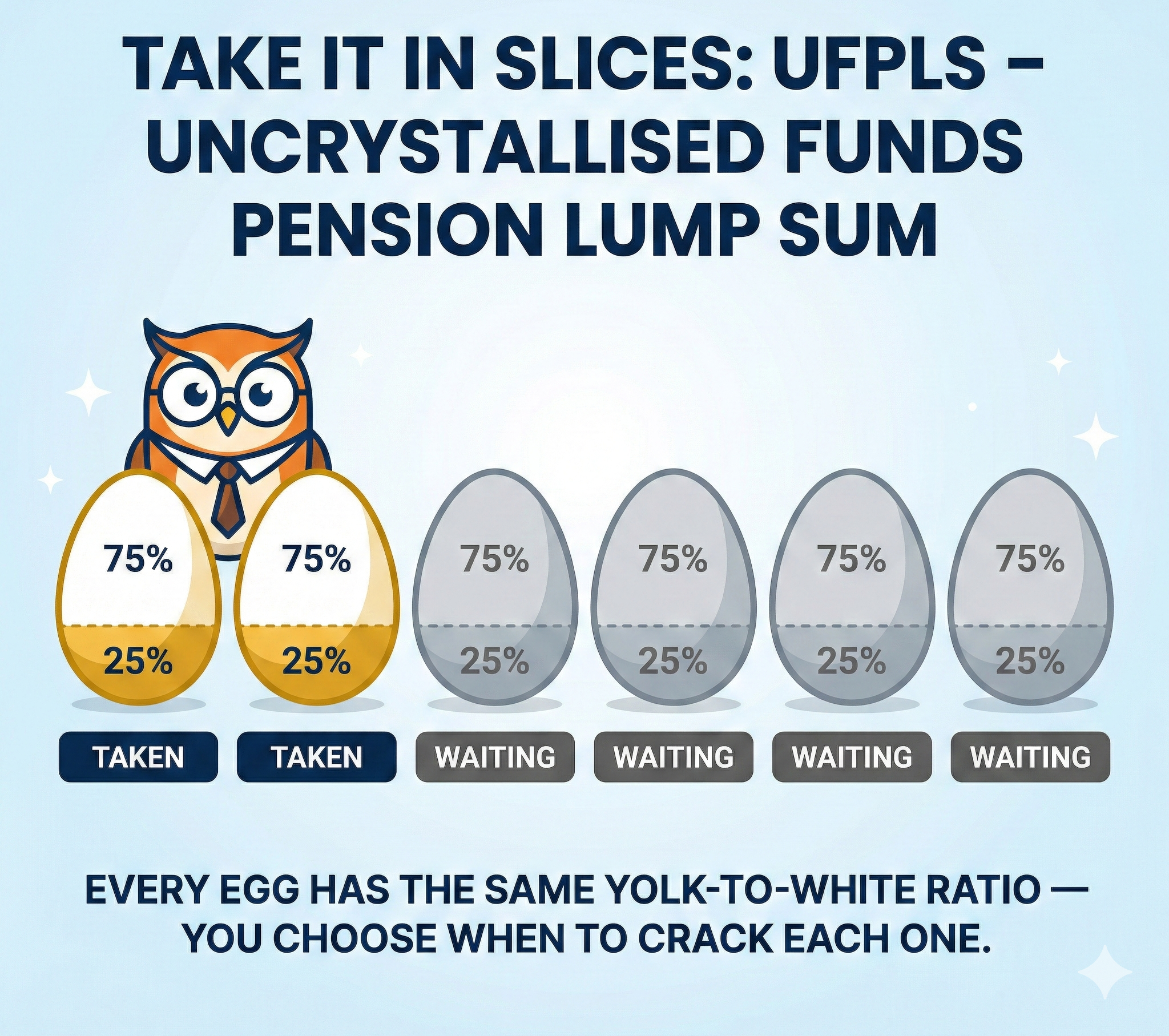

Option 2: Take it in slices (UFPLS)

Take it in slices: Uncrystallised Fund Pension Lump Sum

UFPLS is jargon for a simple thing: you take slices of the cooked egg, one at a time.

Each slice is always:

25% yolk (tax-free)

75% white (taxable)

The rest stays invested, still growing inside the pension wrapper.

MPAA warning (this is one of the biggest “gotchas”)

Because every UFPLS slice includes taxable white, taking UFPLS counts as taking taxable income, so it triggers the MPAA. Once triggered, your future money-purchase pension contributions can be restricted to £10,000 per tax year.

That’s fine if you’re fully retired. It’s a problem if you’re still working and paying in (especially if your employer contributes generously).

Who it’s for: people who want ad-hoc access without setting up drawdown. The trap: you cannot separate yolk and white. Every withdrawal is forced into the 25/75 split.

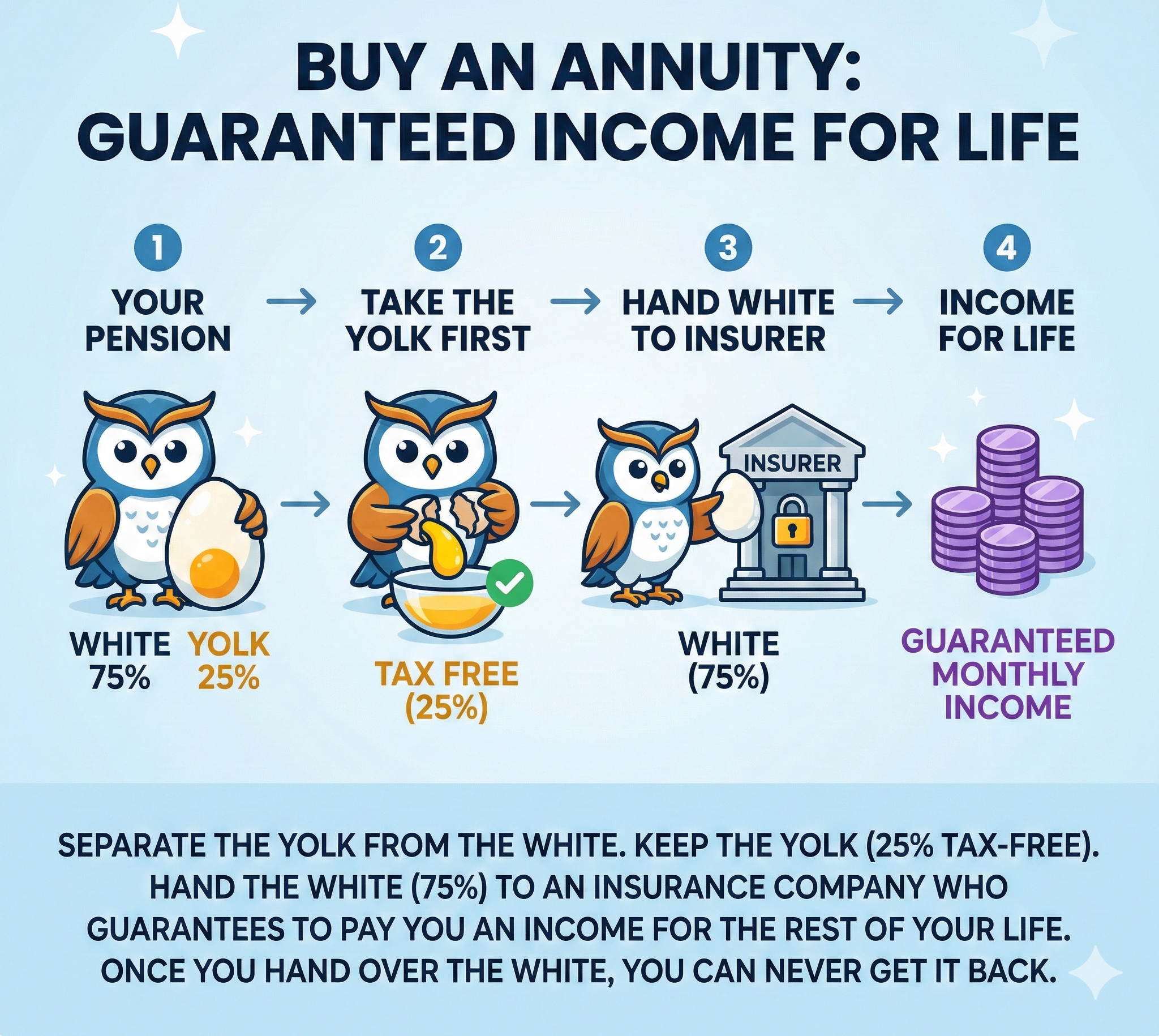

Option 3: Buy an annuity

Buying an annuity: Guaranteed Income for life

This is about certainty.

You:

take your yolk (tax-free cash)

hand your white to an insurer

receive a guaranteed income for life (taxed as income)

Markets crash? Still paid. Live to 105? Still paid. That certainty can be worth real money.

MPAA note (important): annuities don’t trigger it

Buying a lifetime annuity does not trigger the MPAA.

Who it’s for: people who want a guaranteed baseline income. The trap: once you hand the white over, you generally can’t get the capital back. And inflation can erode the spending power of level payments over time.

Option 4: Flexi-access drawdown

Tax free cash first, the drawdown: Flexiaccess Drawdown (FAD)

This is the flexible one.

You separate the egg:

Yolk goes into its own pot (take whenever you like)

White moves into a drawdown bowl (stays invested), and you “dip” income out as needed

Unlike UFPLS, you control the mix:

yolk without white

white without yolk

any combination across tax years

MPAA warning (depends what you actually take)

This is where people slip up.

If you only take yolk (tax-free cash) and no taxable white income, you do not trigger the MPAA.

The moment you take taxable income from the drawdown bowl (white), you trigger the MPAA, and your future money-purchase contributions can drop to £10,000 a year.

So drawdown gives you control, but it also gives you enough rope to accidentally kneecap your future pension contributions.

Who it’s for: most people with meaningful pots who want flexibility and tax planning. The trap: investment risk plus withdrawal rate risk. Take too much, for too long, and the bowl empties.

Option 5: Leave the egg in the nest

Leave it invested: don’t crack the egg. Let it grow.

If you don’t need the income yet, doing nothing can be the smartest move.

Leave the egg alone and you keep:

tax-sheltered growth inside the pension wrapper

full flexibility for later

MPAA note: doing nothing doesn’t trigger it

The MPAA is triggered by taking taxable income. If you leave the pot untouched, there’s no trigger.

The estate planning twist (the rules are changing)

The government has confirmed that from 6 April 2027, unused pensions and death benefits will be brought into scope for Inheritance Tax (with some exclusions).

That doesn’t mean “never leave it invested.” It means the old assumption (”pensions are always outside IHT”) is getting shakier, and planning matters more than ever.

The hidden sting: MPAA in one paragraph

The MPAA is the rule that punishes “just taking a bit” if you’re still building your pension.

The standard annual allowance can be up to £60,000 (subject to tapering). Once the MPAA is triggered, you may be restricted to £10,000 for money-purchase contributions. The MPAA is triggered by taxable income (UFPLS slices, drawdown income, full cash-outs). It is not triggered by annuity purchase or by taking only tax-free cash.

So… which egg strategy is right?

The honest answer: it depends, but not in a hand-wavy way.

It depends on:

your other income and tax bands over multiple tax years

whether you’re still contributing (MPAA risk)

health and longevity

appetite for investment risk versus certainty

whether inheritance planning matters, especially post-2027

If you’re within striking distance of this decision:

use Pension Wise for a free, impartial walkthrough

model withdrawals across several tax years with a financial planner

if your pot is substantial, complicated or overwhelming, consider regulated advice. The cost of getting it wrong is usually bigger than the fee.

General information, not personal advice. Tax rules can change and depend on circumstances. Speak to a regulated adviser before acting.