For years, pensions have been sold as the gold standard of UK wealth-building. Tax relief on the way in. Growth sheltered from tax. Then 25% tax-free on the way out.

And to be fair, pensions are still powerful.

But the pension “deal” is no longer something you can treat as fixed. The real story isn’t one dramatic announcement. It’s the combination of three things working together:

Fiscal drag. Cash limits that don’t move while everything else does.

Inheritance tax creeping towards pensions.

And “25% tax-free” becoming a headline that hides a shrinking cap.

Here’s the uncomfortable bit, most people are modelling their retirement in one currency, while the government is applying the rules in another.

The mismatch that will catch younger savers

Most pension calculators show outcomes in today’s pounds. That’s useful for understanding spending power.

But the rules that limit how much you can take tax-free are set in cash terms. The headline stays the same. The cap is what matters.

The maximum tax-free lump sum for most people is £268,275. That’s 25% of the old Lifetime Allowance of £1,073,100. Once your pension pot gets big enough, the “25% tax-free” promise stops scaling.

So a calculator can tell a 21-year-old: “You’ll have the equivalent of £400k in today’s money.”

And the policy system can still say: “Fine. But in the real world, your cash pot is well past the level where your tax-free cash can keep rising.”

That is pension fiscal drag. Not an accident. A design.

The history tells the story

When the Lifetime Allowance was introduced in 2006, it was set at £1.5 million. That meant 25% tax-free cash of up to £375,000.

It rose steadily, reaching £1.8 million by 2010/11. Tax-free cash peaked at £450,000.

Then came the cuts. George Osborne slashed the Lifetime Allowance three times:

In 2012, it dropped to £1.5 million. Tax-free cash fell to £375,000.

In 2014, down to £1.25 million. Tax-free cash: £312,500.

By 2016, it hit £1 million. Tax-free cash bottomed out at just £250,000.

It crept back up with inflation to £1,073,100 by 2020/21. And there it stayed. Frozen. For four years.

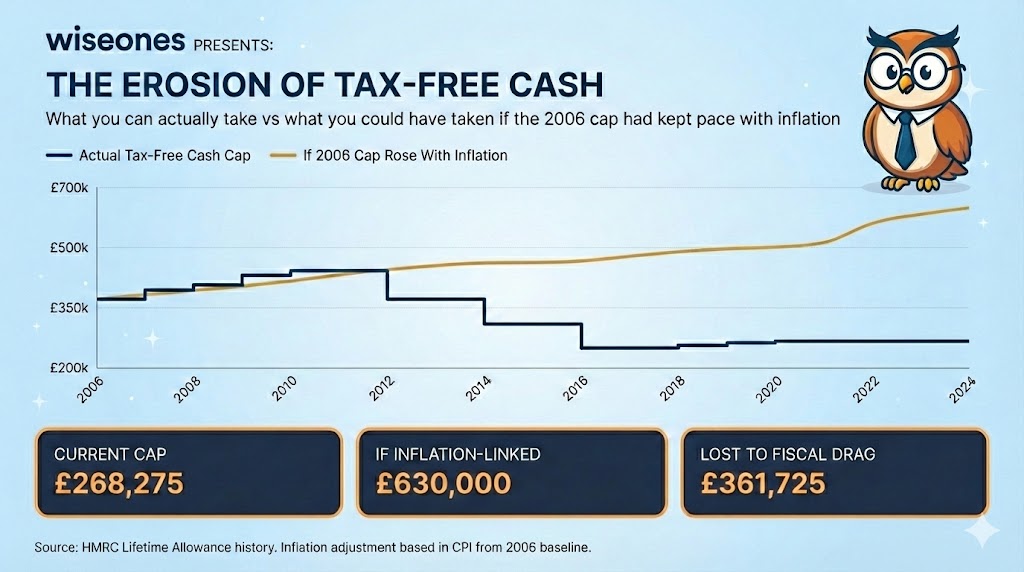

When the Lifetime Allowance was abolished in April 2024, the tax-free cash cap was fixed at £268,275. No mechanism to increase it. No link to inflation. Just a number, set in stone, while everything around it keeps moving.

If the original 2006 cap of £375,000 had simply risen with CPI inflation, it would be worth around £630,000 today.

Instead, you get £268,275.

The gap is £361,725. That’s the cost of fiscal drag.

Fiscal drag isn’t inflation. It’s politics with the volume turned down.

If a Chancellor stands up and says “I’m cutting your pension tax-free cash”, people notice. Newspapers run headlines. MPs get letters.

If a Chancellor stands up and says nothing, but allows limits to stay fixed while wages and prices rise, the effect is similar. It just arrives quietly. Years later, without a single announcement.

We’ve already seen the same approach with income tax thresholds. The personal allowance has been frozen at £12,570 since 2021. The higher rate threshold at £50,270. Every year, more people drift into higher tax brackets without earning more in real terms.

The lesson is simple that fiscal drag is a revenue-raising tool that avoids the pain of a visible tax rise.

And once you see it in income tax, it’s hard not to notice it elsewhere.

Why “25% tax-free” is becoming a weaker promise

The rule has stayed. The ceiling has not.

For earlier generations, pension growth meant more tax-free cash. Build a bigger pot, take a bigger lump sum.

For younger savers, that link is breaking. Pension growth increasingly means more of the pot falling into taxable territory, while the tax-free portion stays capped.

Look at the numbers:

2010 peak: £450,000 tax-free on a £1.8m pot

2016 low point: £250,000 tax-free on a £1m pot

Today: £268,275 tax-free, regardless of pot size

In other words: the better you save, the more likely you are to collide with a cash limit that was never built to run alongside decades of compounding.

This is no longer a “high earner problem”

Let’s make this practical.

Take someone who starts work at 21, contributes 10% of a £35,000 salary every year, and sees their pension grow at 7% annually. Retire at 67.

That’s 46 years of compounding. Even with modest assumptions, you’re looking at a pension pot comfortably over £1 million in nominal terms.

At that point, the “25% tax-free” promise delivers £268,275. Not 25% of your pot. Just the cap.

Allow for normal pay progression over a working life, and the number of people drifting into that zone only rises.

This isn’t about high-flyers with massive pensions. It’s about long careers, decent consistency, and time.

Inheritance tax and pensions: a second squeeze

For years, pensions were the place you might leave money. They sat outside the normal inheritance tax story. Pass on your pension, and your beneficiaries could often receive it without IHT applying.

Now the direction of travel is different.

From April 2027, most pension wealth will be brought into the inheritance tax net. The same saver may face a capped tax-free cash outcome in retirement and fewer inheritance planning advantages than previous generations assumed.

Again, not one dramatic announcement. More like a steady narrowing.

And the state may make it harder to contribute efficiently

Salary sacrifice has been one of the most effective ways to fund a pension. Reduce your income before tax and NICs. Improve efficiency. Sometimes share employer NIC savings.

But the direction of policy is towards limiting that advantage too.

Wiseones view: When governments start tightening the “how”, it’s usually because they’ve already decided the “why”. Pensions are still encouraged, but the most generous edges are politically easy to trim.

So is it still worth it?

Yes. For most people, pensions remain a cornerstone.

But the strategy has to mature.

If you’re younger, the risk isn’t “pensions won’t work”. The risk is that you build everything inside one wrapper, then discover the wrapper is being quietly tightened in ways you can’t easily respond to at 58.

The Wiseones question isn’t “pension or no pension.”

It’s this:

How much pension is enough before flexibility matters more?

How do you balance pensions with ISAs and other investments so policy change can’t trap you?

What does “tax-free” really mean when there’s a ceiling that doesn’t rise with life?

Because fiscal drag is rarely an accident.

It’s politics with the volume turned down.

This article is for general information purposes only and does not constitute regulated financial advice. The value of pensions and investments can fall as well as rise. Tax treatment depends on individual circumstances and may change. Consider seeking independent financial advice before making decisions about your pension.

This is why financial planning is not a set it and forget it. Policy changes and wrappers change, keep planning each year to stay ahead of the curve.