Risk questionnaire versus a good adviser

At its best, financial advice has always been a personal relationship.

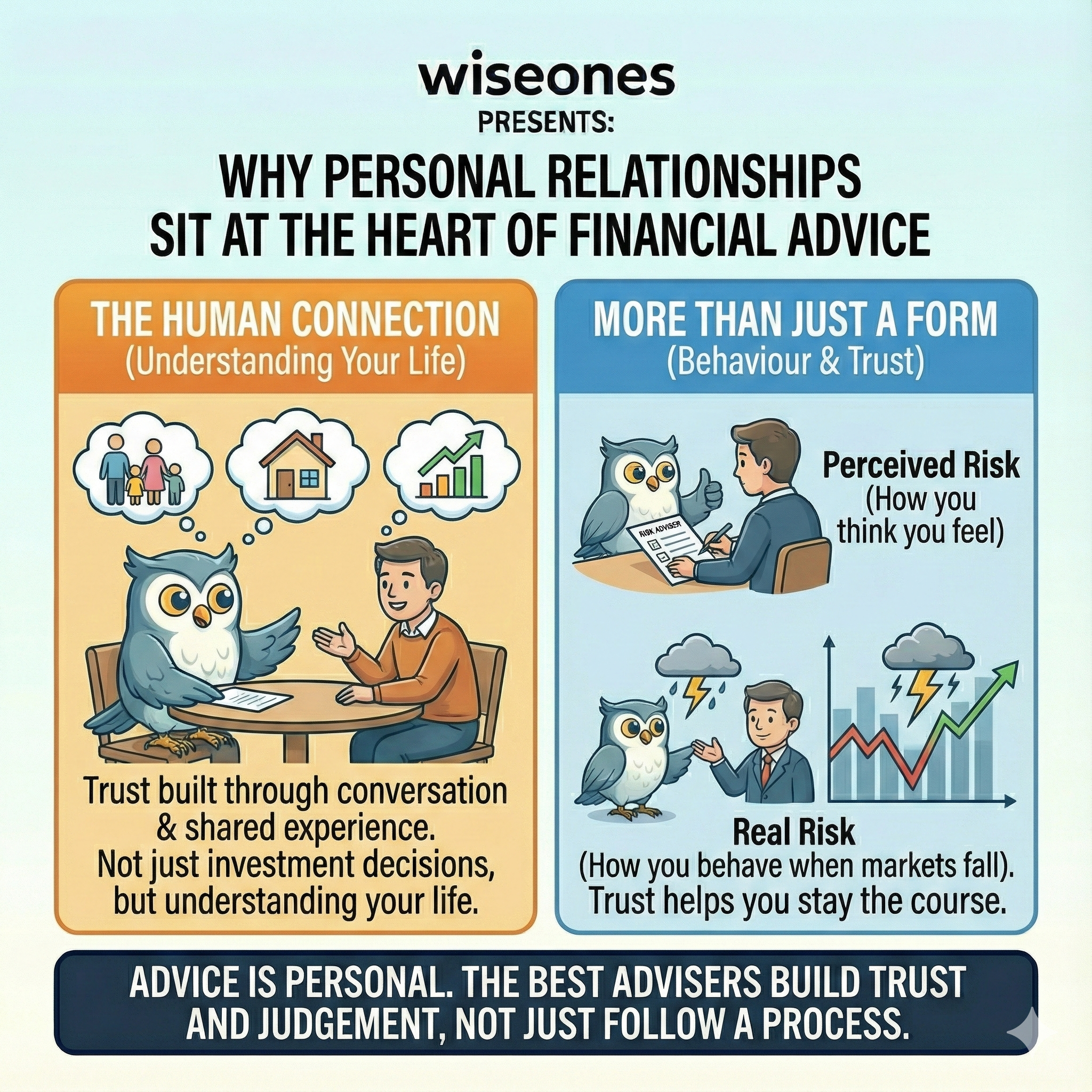

When you work with a good adviser, you aren’t just outsourcing investment decisions. You’re placing trust in someone who understands your life, your family, your work, your ambitions, and your anxieties about money. Over time, that adviser builds a deep understanding of how you respond to uncertainty, not just how markets behave in theory.

That kind of knowledge can’t be captured in a form or fully transferred to someone new. It’s built slowly, through conversation, shared experience, and trust.

And it matters far more than most people realise.

Perceived Risk and Real Risk Aren’t the Same Thing

This is where the psychology of investing comes in.

Venture capitalist Bill Gurley summed it up perfectly when speaking on Tim Ferriss’s podcast:

“Your actual risk tolerance may differ from your perceived risk tolerance.”

Risk questionnaires can tell you how someone thinks they feel about risk.

They rarely tell you how that person will behave when markets fall sharply.

That only becomes clear over time and usually only through a trusted adviser relationship.

Why This Will Matter in the Next Downturn

In rising markets, these differences are easy to ignore.

Most investors feel comfortable when portfolios are growing. Risk feels theoretical. Long-term plans feel obvious. Advice can seem almost unnecessary.

It’s during drawdowns that reality sets in.

When markets fall significantly, clients don’t just need performance updates or generic reassurance. They need context. They need someone who understands their circumstances well enough to explain:

why this was expected

why it feels uncomfortable

why the plan still makes sense

Without that personal connection, even well-constructed portfolios can unravel — not because of poor investments, but because confidence disappears at exactly the wrong moment.

How Consolidation Has Changed the Nature of Advice

Over the past decade, the structure of the advice industry has shifted dramatically.

Small, owner-managed firms have increasingly been absorbed into large national consolidators, many backed by private equity. Rising compliance costs, regulatory complexity, and attractive exit valuations have made selling up a rational decision for many advisers.

In some cases, firms have been acquired for values equivalent to around 8% of assets under management, as seen in consolidator-led models such as True Potential.

To put that into perspective, a typical ongoing adviser charge might be around 0.75% per year. An 8% valuation represents more than ten years of future advice fees paid upfront.

That capital has to be recovered somewhere and over time, it influences how advice is delivered.

As firms scale, advice often becomes more systematic: centralised investment models, standardised risk frameworks, interchangeable advisers, and reduced continuity of contact.

This doesn’t reflect badly on individual advisers. But it does change the nature of advice. Trust becomes institutional rather than personal. Knowledge becomes recorded rather than lived.

The Shift From Incentives to Forms

It’s worth remembering how we got here.

Before the Global Financial Crisis, commission-driven advice created real problems. Incentives were often misaligned, and some advisers sold whatever paid the most. Reform was needed, leading to the creation of the Financial Conduct Authority and the removal of commission-based advice.

But over time, the pendulum has swung too far the other way.

Advice is increasingly driven by compliance frameworks and attitude-to-risk questionnaires, especially in the systematic consolidators. These tools were designed to protect clients, but in practice they often protect firms. No adviser is ever criticised for lowering risk to match a questionnaire score. Right? Especially if that score can be pointed to later to defend against a complaint. Judgement gives way to process. Suitability becomes defensibility.

Advice is personal. You wouldn’t go to a therapist and expect a tick-box survey to replace a conversation. Financial advice, which deals with people’s futures, shouldn’t be reduced to a form either.

Independent and Restricted Advice

Understanding the Differences

Not all advisers operate under the same framework, and the distinctions matter.

Independent advisers

Whole of market access

Broad and flexible product choice

External funds and models

Highly tailored advice

Strong continuity of relationship

Restricted advisers

Limited product or provider range

Defined, often platform-led solutions

Frequently in-house models

More standardised advice

Continuity can vary if a consolidator

Great Advisers Exist in Every Model

A great adviser is still a great adviser, whether they operate independently or within a restricted framework.

The best advisers bring judgement, empathy, experience, and calm. They explain clearly. They prepare clients for uncertainty. They stay engaged when markets are uncomfortable. And they build trust over time.

Structure influences how advice is delivered but it doesn’t create or destroy talent.

The real question is whether the firm allows great advisers to remain great.

Do systems support relationships, or replace them?

Does scale free up adviser time, or consume it?

Does the business protect continuity, or treat advisers as interchangeable?

Firms that recognise the value of personal relationships and design around them will stand out. Those that don’t may only discover the cost when markets turn.

Looking Ahead

The future of financial advice doesn’t need to be more transactional, it needs to be more human.

As technology and AI take over more of the administrative burden, the best firms will use that opportunity to give advisers more time with clients, not less.

Because when markets are calm, advice can feel optional.

When markets fall, having a trusted adviser who understands both your finances and your psychology becomes invaluable.