Guidance & advise, Wealth manager & financial planner…

Most people don’t ignore financial planning because they don’t care.

They avoid it because it feels complicated, full of jargon, or designed for someone wealthier than them.

Financial planning is not about predicting the future or picking the perfect investment. It is about making better decisions with the information you have today, understanding trade-offs, and avoiding mistakes that quietly compound over time.

This guide explains the foundations: the difference between guidance and advice, what financial planning really means, how advisers fit into the picture, and the wider areas, like family protection and estate planning that are often overlooked.

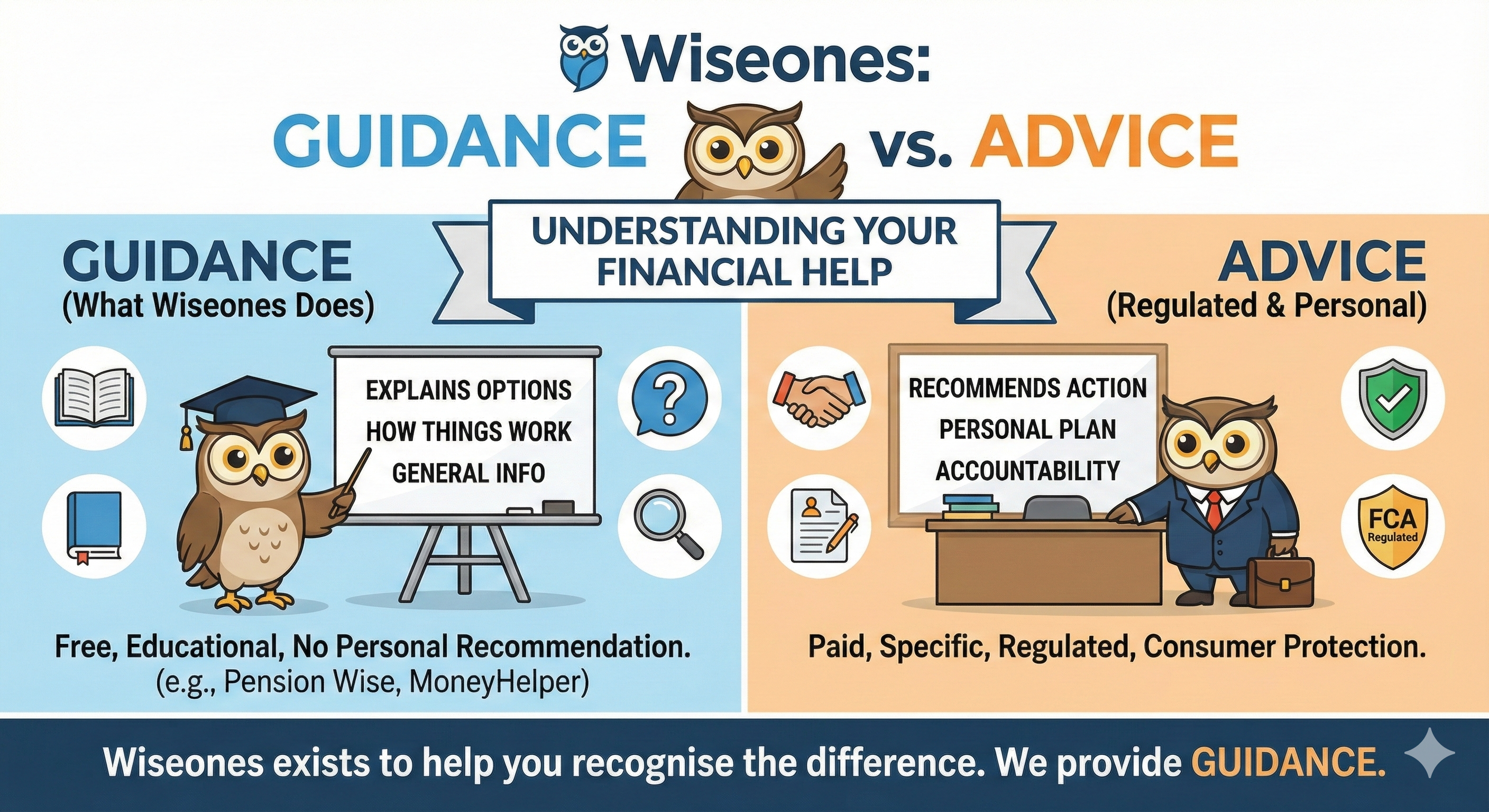

Financial Guidance vs Financial Advice

Let’s start with a distinction that underpins everything.

Financial Guidance

Financial guidance helps you understand your options. It explains how things work, what choices exist, and what questions you might want to ask.

Guidance can help you learn:

How pensions work and how they’re taxed

What different investment risks actually mean

How ISAs differ from pensions

What typically matters at different stages of life

What guidance does not do is tell you what you personally should do.

Because it’s general and educational, guidance is often free and carries no responsibility for outcomes. That is exactly what we at Wiseones are here to do.

In the UK, high-quality guidance is also available if you’re over 50 and approaching pension decisions through Pension Wise, which offers one-to-one guidance with a trained specialist.

Financial Advice

Financial advice is different. Advice is personal.

If someone considers your income, family, goals, pensions, savings, and tolerance for risk and then recommends a specific course of action. That is financial advice. It is regulated, comes with accountability, and is designed to protect consumers when decisions carry real consequences.

A simple way to think about it:

Guidance explains

Advice recommends

Wiseones focuses on the first, while recognising when the second can be extremely valuable.

Financial Planner vs Wealth Manager

These terms are often used interchangeably, which can cause confusion. While there is overlap, they are intended to serve different purposes.

Financial Planner

Financial planning is a big-picture process. It looks at how all parts of your financial life fit together over time.

Good financial planning considers:

Income and spending

Short- and long-term goals

Pensions and retirement

Investments

Tax efficiency

Protection for life’s “what ifs”

Family and estate considerations

At its core, financial planning asks:

“What do I want my money to do for my life?”

Wealth Manager

Wealth management is usually narrower and more investment-focused. It tends to centre on managing portfolios and asset allocation, often for people with significant capital.

Wealth management can be part of a financial plan, but without planning, investments risk becoming disconnected from real-life goals.

A small caveat: the terms are often used interchangeably. Some wealth managers are also financial planners, and many financial planners provide wealth management services. As a rule of thumb, both will be regulated financial advisers, the difference is usually emphasis, not regulation.

What a Financial Adviser Actually Does

A financial adviser’s role is not to beat the market or sell products. At its best, it is about structure, clarity, and judgement.

A good adviser helps people:

Prioritise competing goals

Avoid emotional decisions during uncertainty

Make sense of complex rules around tax and pensions

Adjust plans as life changes

Make sure the advice you get is suitable

In the UK, advisers who provide personal recommendations must be authorised and regulated by the Financial Conduct Authority, which provides consumer protections and accountability.

The Core Building Blocks of Financial Planning

1. Cash Flow Thinking

At the heart of planning is understanding cash flow over time, not just what you earn today, but how money moves through your life.

This helps answer questions like:

What happens if I retire earlier or later?

How much flexibility do I really have?

What risks could derail my plans?

Clarity here often reduces anxiety more than any investment choice.

2. Investments in Context

Investments are tools, not goals.

What matters is:

When you’ll need the money

How much uncertainty you can tolerate

Whether growth, income, or stability matters most

The “right” investment depends on timing and purpose, not headlines or past performance.

3. Understanding Risk (Emotionally, Not Just Mathematically)

Risk isn’t just numbers on a chart. It’s how you react when markets fall, plans change, or uncertainty appears. A good adviser will spend a lot of time explaining this.

A thoughtful approach to risk balances:

What you need to achieve

What you can afford to lose

How you are likely to feel during downturns

When Paying for Advice Makes Sense

Advice is usually worth considering when:

Decisions are complex or irreversible

Pensions, tax, or inheritance are involved

You want accountability, not just information

The cost of getting it wrong is high

Guidance is often enough when:

You’re learning the basics

Exploring options

Making lower-impact decisions

Wiseones exists to help you recognise the difference.

One-Off Fees vs Ongoing Advice Fees

How advice is paid for matters and it’s something many people don’t fully understand.

A one-off charge typically pays for a snapshot in time. It covers advice based on your circumstances as they are right now. This can be useful for a specific decision or review, but it does not adapt automatically as life, markets, or legislation change.

An ongoing fee pays for an ongoing service. This usually includes:

Regular reviews

Monitoring investments

Adjusting plans as your family and circumstances change

Ongoing assessment of suitability as rules and markets evolve

In simple terms:

One-off advice answers “What should I do now?”

Ongoing advice focuses on “Are we still on track, is this still suitable and does this still make sense?”

Neither is inherently right or wrong. The value depends on complexity, confidence, and how much ongoing support you want.

Looking Beyond Investments: Family, Protection, and Estate Planning

Financial decisions rarely affect just one person.

Protection Planning

Life insurance, critical illness cover, and income protection exist to protect lifestyles and families. These areas are often neglected because they’re uncomfortable to think about, yet they underpin long-term financial resilience.

Estate and Inheritance Planning

Estate planning is not just about tax. It’s about clarity, fairness, and reducing stress for those you leave behind.

This includes:

Having an up-to-date will

Reviewing pension beneficiaries

Understanding how assets pass on death

Considering lifetime gifts and longer-term planning

Pensions, in particular, can be powerful estate-planning tools when understood properly.

Trusted Sources of Free UK Guidance

If you want impartial, government-backed help:

MoneyHelper – support with pensions, savings, debt, and money decisions

Pension Wise – free guidance for over-50s approaching pension choices

A Wiseones Checklist: Things Worth Thinking About

Do I know where my money is actually going?

What decisions will matter most in the next 5–10 years?

Do I understand my pensions well enough?

What happens financially if life doesn’t go to plan?

Have I thought beyond investments alone?

Do I know when guidance is enough and when advice matters?

Wiseones Disclosure – Read This First

Wiseones is financial guidance providing general financial information and education only. Content published here is designed to improve understanding and awareness and does not constitute regulated financial advice or a personal recommendation.

All information is generic and does not take account of individual circumstances. Tax, pension, and legislative references are based on UK rules at the time of writing and may change in the future.

Investments can fall as well as rise in value. Past performance is not a reliable indicator of future results.

Where personal recommendations are required, readers should seek advice from a financial adviser authorised and regulated by the Financial Conduct Authority.

For free, impartial guidance, readers may also wish to visit MoneyHelper or Pension Wise.