You’ve got the wrapper. You’ve been told it’s “tax efficient.” Gold star.

But what’s actually inside it? Can you stick crypto in your pension? Shares in your ISA? A rental flat in your SIPP? (Spoiler: please don’t try that last one.)

Most people never think about this stuff. They open an account, pick a fund that sounds sensible, and hope for the best. Nothing wrong with that. But if you want to make the most of what’s available, it helps to know what each wrapper can actually hold.

Consider this your cheat sheet.

Quick Refresher: What Is a Wrapper?

Think of it like a lunchbox. The lunchbox has its own rules. How much you can put in. When you can open it. Whether the taxman gets to peek inside.

But the food is the interesting bit. Shares, bonds, funds, property, crypto. The same investment can sit in completely different wrappers and be treated very differently by HMRC.

Same sandwich. Different lunchbox. Different tax bill.

Let’s open them up.

Pensions (Workplace or SIPP)

The big one. Money goes in, gets tax relief, and stays locked up until at least age 55 (rising to 57 from April 2028). In return, your investments grow completely free of income tax and capital gains tax while they’re inside.

What you can invest in depends entirely on your pension type. And the range is enormous.

A basic workplace scheme like Nest gives you roughly zero choice. You’re in a default fund. That’s it. Don’t like it? Tough. Move up to providers like Aviva, Royal London, or Scottish Widows and the menu opens up to a few hundred funds. Some advanced workplace pensions through Aegon can even unlock full SIPP functionality, meaning thousands of options.

A proper Self-Invested Personal Pension (SIPP) is the full buffet. Individual shares on global exchanges (including AIM), ETFs, bonds, gilts, funds, and even commercial property if your provider allows it. Since October 2025, crypto ETNs have been on the table too. And for experienced investors, Long-Term Asset Funds (LTAFs) now sit in SIPPs as well, giving access to private equity, infrastructure, and real estate. They’re classed as non-standard investments though, so your provider needs to hold extra capital.

Then there’s the SSAS. That’s for business owners (maximum 11 members), and it opens up even more specialist territory: lending money back to your own company, buying commercial property with borrowing. We’ll cover that separately.

Stocks and Shares ISA

Everyone’s favourite. Up to £20,000 per year, and everything inside grows and comes out completely tax-free. No income tax on dividends. No capital gains tax when you sell. Nothing. Nada.

The investment range is solid: shares on recognised exchanges, funds (unit trusts and OEICs), investment trusts, ETFs, and government and corporate bonds. Narrower than a SIPP, but more than enough for most people. No direct property, no alternatives, no commercial lending.

Here’s where it gets interesting. Until April 2026, you can hold crypto ETNs in a Stocks and Shares ISA. After that, they’re moving house to the Innovative Finance ISA. Meanwhile, heading in the opposite direction, LTAFs will become eligible for Stocks and Shares ISAs from April 2026. Private markets in an ISA. That’s new.

Innovative Finance ISA (IFISA)

The quiet one at the back of the classroom. Originally built for peer-to-peer lending, it’s been slowly picking up new residents.

You can hold crowdfunded bonds through providers like Triodos. And from April 2026, crypto ETNs will move in here. That might finally give this wrapper its moment.

Same £20,000 annual limit as all ISAs (shared across the lot). Not many people have one yet. That could change.

One thing to flag. IFISAs are not covered by the FSCS. If your P2P platform goes bust, your money could go with it. Higher potential returns come with higher risk. Eyes open, please.

Onshore Investment Bond

Right, we’re getting into specialist territory now. Stay with us, it’s worth it for some of you.

An onshore investment bond is issued by a UK life insurance company. Technically it’s a life insurance policy. In practice, it’s an investment wrapper with some genuinely clever tax tricks.

You invest a lump sum into a range of funds (unit trusts and OEICs), investment trusts, ETFs, and cash. Some providers like HSBC Life offer over 3,800 fund options including ETFs. That’s broader than most people expect. .

You’re treated as having already paid basic rate tax. If you’re a basic rate taxpayer when you eventually cash in, there might be nothing more to pay. Higher rate taxpayers will face a bill, but there are planning tools to help.

The headline feature is the 5% annual withdrawal allowance. You can take out up to 5% of your original investment each year for 20 years without triggering an immediate tax charge. Don’t use it one year? It rolls forward. Very handy for drip-feeding income in retirement and deferring tax payment.

You can switch between funds inside the bond without creating a personal tax event. No CGT on switches. Rebalance to your heart’s content.

And here’s the kicker. No contribution limit. These sit completely outside your ISA and pension allowances.

Offshore Investment Bond

Same idea, sunnier postcode. Issued by a life company based outside the UK, usually the Isle of Man, Ireland, or the Channel Islands.

The big difference is gross roll-up. No tax is paid on the growth inside the bond while it’s invested. Not corporation tax. Not income tax. Nothing. Your money compounds without the annual drag of taxation, which over the long term can make a real difference to the size of your pot.

The investment range is broadly similar to onshore: funds, investment trusts, ETFs, REITs, and cash. Some providers also allow discretionary investment managers (DIMs) to hold direct equities and bonds within the insurer’s internal linked fund structure. That widens the menu without triggering problems.

Now, here’s the bit that catches people out.

HMRC keeps a strict list of permitted property categories (under S520 ITTOIA 2005) that you’re allowed to select. The list covers funds, OEICs, unit trusts, investment trusts, REITs, cash, and a handful of others. Step outside it and the bond gets reclassified as a Personal Portfolio Bond (PPB). That triggers a whole new world and it is brutal stuff. The workaround is to invest through the insurer’s own internal funds or use a DIM who operates within the insurer’s structure. If anyone ever mentions PPB rules to you, sit up and listen.

Offshore bonds also get the 5% withdrawal allowance and have no contribution limit. They tend to show up in planning for trusts, estates, or people who spend time abroad (where time apportionment relief can reduce the UK tax bill on gains made while non-resident).

General Investment Account (GIA)

The GIA is the “everything else” account. No tax wrapper. No shelter. No annual limit. Just a straightforward investment account where you hold whatever you like: shares, funds, ETFs, bonds, direct crypto, alternatives. The full works.

The catch? You’ll pay tax on dividends, interest, and capital gains as they arise.

Think of it as the default. If an investment doesn’t fit inside any of the wrappers above, it ends up here.

But don’t write off the GIA just yet. It’s got a trick.

Bed and ISA

This one’s a proper hidden gem for anyone with investments sitting in a GIA.

Bed and ISA means selling investments in your GIA and immediately rebuying the same ones inside your ISA. Simple as that.

Why bother? Because investments in a GIA are exposed to capital gains tax (the annual exempt amount is just £3,000 per person, or £1,500 for most trusts) and dividend tax (allowance down to £500). Move them into an ISA and all future growth and income become completely tax-free. Forever.

You can’t just transfer shares directly. HMRC won’t have it. You sell, move the cash, rebuy. Most major platforms (AJ Bell, Hargreaves Lansdown, interactive investor, Fidelity) now have a one-click Bed and ISA option that does the whole thing in one go.

A few things to know. You’re briefly out of the market during the trade, so there’s a small risk of price movement. You might get back slightly fewer shares because of the bid-offer spread and dealing costs. And if the investments you sell have gains above your £3,000 CGT allowance, you’ll owe tax on the excess. Couples can transfer assets between them tax-free first to double up on the allowance.

Small prices to pay for getting investments into a tax-free home permanently. If you’ve got money in a GIA and unused ISA allowance, this should be near the top of your annual to-do list. You can do a Bed and SIPP using the same approach too.

The Crypto Question

This is the bit that’s changing fast.

Until October 2025, UK retail investors couldn’t buy crypto exchange-traded notes (ETNs) at all. The FCA had banned them since January 2021. That ban has now been lifted.

A crypto ETN is a listed product that tracks the price of a cryptocurrency (typically Bitcoin or Ethereum) without you ever owning the coins directly. They trade on exchanges just like shares. No wallet needed. No private keys. No dodgy exchange accounts.

Several are now listed on the London Stock Exchange from the likes of BlackRock (iShares Bitcoin ETP), WisdomTree, 21Shares, and Bitwise. All physically backed by actual crypto held with regulated custodians. Fees sit around 0.10% to 0.35%, which is competitive with traditional ETFs.

Here’s how they work across the wrappers.

SIPP: Yes. Crypto ETNs qualify as exchange-traded securities, so most SIPPs allow them. Tax-sheltered growth with tax relief on the way in. Currently the cleanest long-term route for regulated crypto exposure.

Stocks and Shares ISA: Yes, but only until April 2026. After that, new crypto ETN purchases move to the IFISA.

IFISA: From April 2026, this becomes the ISA home for crypto ETNs. Not many people have one yet, so expect a wave of account openings.

Investment Bonds: No. Crypto ETNs don’t sit within the permitted investment categories for onshore or offshore bonds.

GIA: Yes. No restrictions, but no tax shelter either. CGT applies on gains above your allowance.

A few important caveats. Crypto ETNs are not covered by the FSCS. They’re classed as complex, high-risk products. You don’t own the underlying crypto. You own a debt note issued by a financial institution that promises to pay you a return linked to the crypto price. If the issuer fails, the note could become worthless. The FCA has been very clear: don’t invest unless you can afford to lose everything.

For people who want a small, regulated crypto allocation inside a tax-efficient wrapper, this is genuinely new territory. We’ll do a deeper piece on this soon.

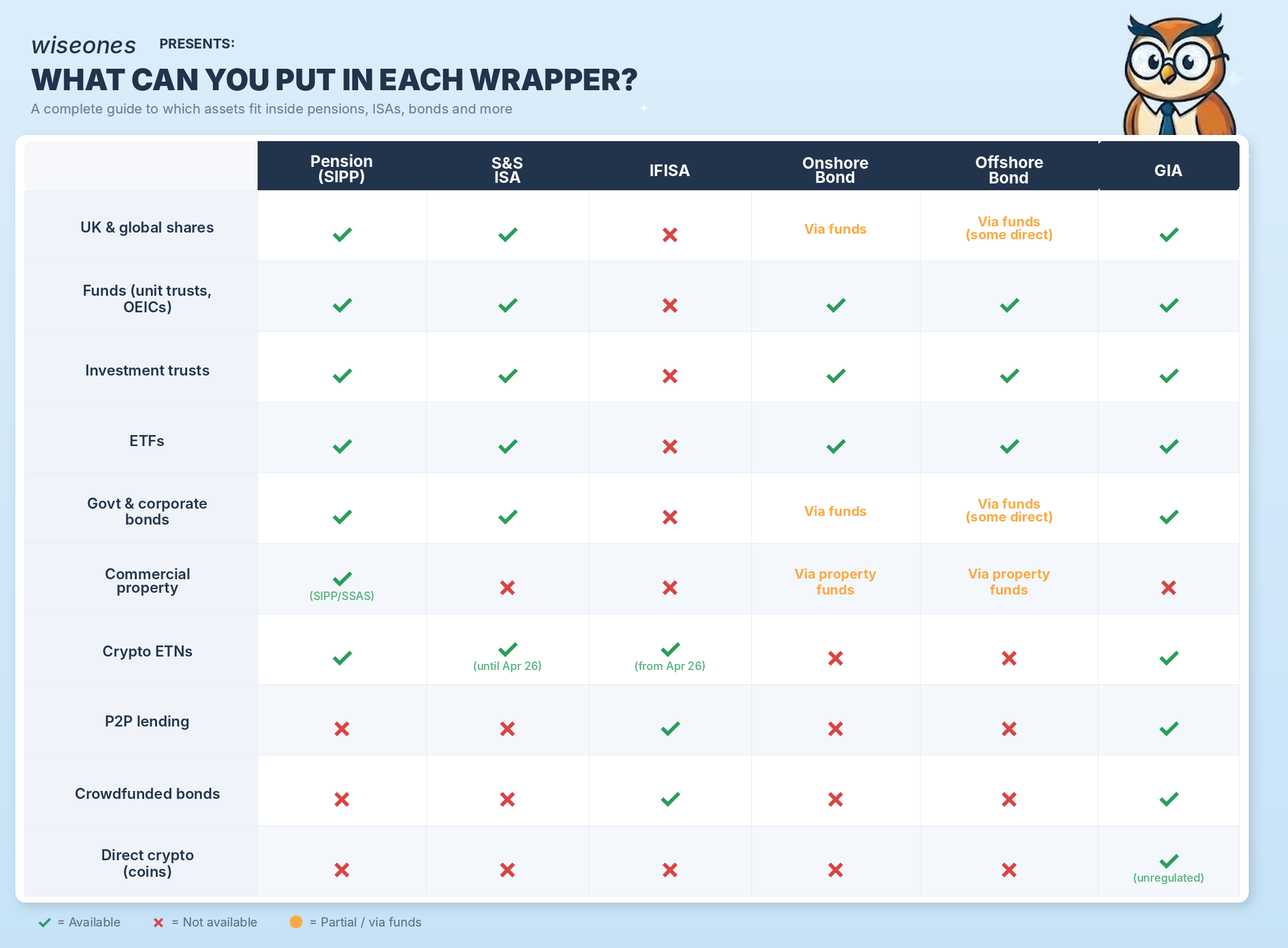

What Can Go Where?

Here’s the full picture. Which assets fit in which wrappers, with the key tax and access details underneath.

That’s the map. We’ll be digging into each wrapper in detail. If there’s one you’d like us to tackle first, let us know.

The Wiseones Summary

The wrapper you choose matters. But so does what you put inside it.

Pensions give you the widest investment menu, especially through a SIPP, and the best tax relief on the way in. The trade-off is your money is locked away until at least age 55. ISAs are more limited on what they can hold but everything comes out completely tax-free and you can access it whenever you like. Investment bonds are the specialist tool, best suited for lump sum planning, income in retirement, or estate work, and they come with their own quirks around permitted investments and tax treatment. The GIA holds anything but shelters nothing, so use your Bed and ISA trick each year to move what you can into a tax-free home.

The big changes to watch? Crypto ETNs are now available in pensions and ISAs. LTAFs are opening up private markets to mainstream wrappers from April 2026. And with the CGT allowance stuck at just £3,000, the case for using your wrappers properly has never been stronger.

Know what you own. Know where you own it. That’s the starting point for everything else.