Pensions get talked about constantly, but often in ways that manage to be both vague and overwhelming at the same time.

“Save for your future.” Sure. But what does that actually mean? When can you touch it? What’s this 25% tax-free thing people mention? And why does everyone seem slightly nervous about something called the MPAA?

This guide breaks down how pensions actually work, the ages, the tax relief, the withdrawals, the traps to avoid and the changes coming down the track. Whether you’re decades from retirement or can see it on the horizon, understanding these rules can make a real difference. This is a long one, but worth making your way through it.

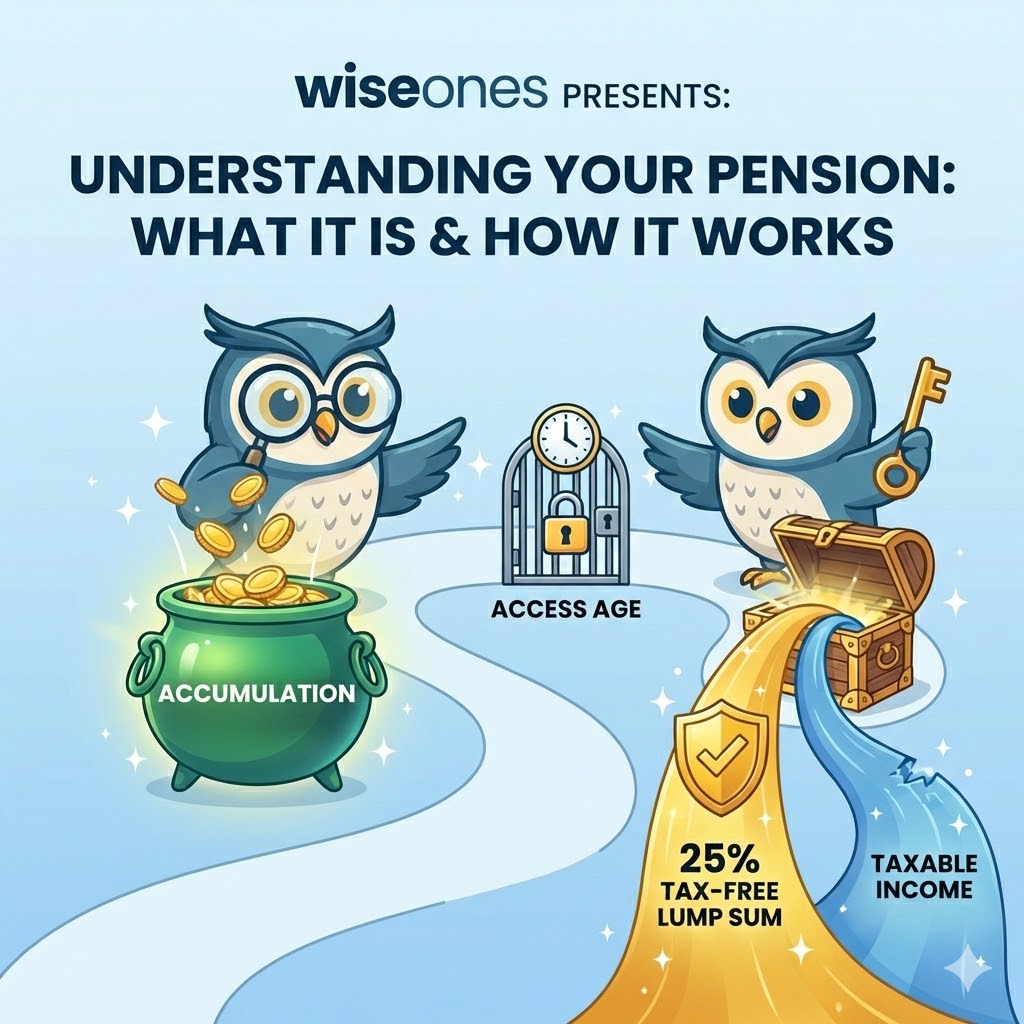

When Can You Actually Access Your Pension?

Let’s start with the basics. Your pension isn’t just locked away forever, but it is locked away for quite a while.

The Normal Minimum Pension Age

Right now, the earliest you can access a private or workplace pension is age 55. This is called the Normal Minimum Pension Age, or NMPA.

But here’s the thing: it’s changing.

From 6 April 2028, the minimum age rises to 57. If you were born after 5 April 1973, this affects you. Those retirement-at-55 plans might need adjusting.

The logic behind this is that the government wants to keep pension access roughly ten years before State Pension age. Speaking of which…

Protected Retirement Ages

Some people have a protected pension age that allows them to access their pension earlier than the standard minimum. This typically applies to:

Certain occupational schemes (armed forces, police, firefighters)

Scheme rules that already provided for earlier access before legislation changed

Some older pension contracts that locked in a lower retirement age

Here’s the crucial bit: if you transfer a pension with a protected retirement age to a new scheme, you may lose that protection.

This matters a lot if you’re thinking about consolidating your pensions. That old workplace pension gathering dust might have a protected age of 50 or even younger. Transfer it to a shiny new SIPP, and that protection could vanish.

Before consolidating any pension, always check whether it has a protected retirement age. If it does, think carefully about whether giving that up is worth the benefits of consolidation. Sometimes keeping an old pension separate makes sense purely to preserve early access rights.

State Pension Age: A Separate Timeline

Your State Pension is different. You can’t touch it until you reach State Pension age, which is currently 66 for everyone.

That’s also changing. From May 2026, State Pension age starts creeping up to 67, completing the transition by March 2028 for those born on or after 6 April 1960. Further increases to 68 are planned for the 2040s, though these timelines get reviewed regularly.

So if you’re planning to stop work at 57 and coast until State Pension kicks in, you’ll need your private pension (and other savings) to bridge that gap. That could be a decade or more.

The 25% Tax-Free Cash: What You Need to Know

This is the bit everyone likes hearing about.

When you access your pension, you can typically take 25% of your pot tax-free. No income tax. Just yours.

The remaining 75%? That gets taxed as income when you withdraw it. But that 25%? It’s one of the most valuable tax perks in UK financial planning.

But There’s a Cap

Here’s where it gets more technical.

Since April 2024, the old Lifetime Allowance has been replaced by two new limits:

The Lump Sum Allowance (LSA) caps the total tax-free cash you can take across all your pensions at £268,275. That’s 25% of the old £1,073,100 Lifetime Allowance.

If you have a pension pot of, say, £1.5 million, then 25% would be £375,000. But you can only take £268,275 tax-free. The rest gets taxed as income.

The Lump Sum and Death Benefit Allowance (LSDBA) is set at £1,073,100 and covers tax-free lump sums during your lifetime plus certain death benefits. This becomes important when we talk about passing pensions on.

Protected Tax-Free Cash

Some people have protected allowances from when the old Lifetime Allowance was repeatedly reduced over the years. If you applied for Primary Protection, Enhanced Protection, Fixed Protection, or Individual Protection back in the day, you might have access to higher tax-free amounts.

The deadline to apply for most of these has passed, but if you think you might have protection, check with your provider. It could be worth a lot.

Do You Have to Take It at 55 (or 57)?

No. Absolutely not.

There’s no requirement to access your tax-free cash at the minimum age. You can leave your pension invested and let it grow. The longer it compounds, the bigger the pot, the bigger your 25% becomes (subject to the cap).

Of course, investments can go down as well as up. But there’s no rush to touch it just because you legally can.

Is There a Maximum Age?

There’s no legislative requirement to take your tax-free cash by a certain age. HMRC doesn’t force you to access it.

However and this is important many pension scheme rules require benefits to be taken by age 75. This is particularly common with older pension contracts. Some schemes simply won’t allow you to take tax-free cash after 75.

Even if your scheme does allow it, there’s a catch: if you die after 75 without having taken your tax-free cash, your beneficiaries won’t get it tax-free. They’ll pay income tax at their marginal rate on the full amount.

So while you’re not legally required to take it, there are good reasons to check your scheme rules as you approach 75. If your current scheme doesn’t offer the flexibility you need, transferring to a more modern arrangement might be worth considering, but get advice first, as transfers aren’t always straightforward.

Making Withdrawals: Your Options Explained

Once you reach pension age, you have choices about how to take your money. This matters more than most people realise, because different methods have different tax consequences.

Option 1: Flexi-Access Drawdown

This is what most people end up using for modern defined contribution pensions.

You take your 25% tax-free cash (all at once or in stages), and the remaining 75% stays invested. You can then withdraw income whenever you want, however much you want. Complete flexibility.

The money left invested can keep growing, but it can also fall. You’re still exposed to market risk.

Key point: If you take only your tax-free cash and don’t withdraw any taxable income, you don’t trigger the MPAA (more on this shortly). This is important if you’re still working and contributing to a pension.

Option 2: Buy an Annuity

An annuity uses your pension pot to buy a guaranteed income for life from an insurance company. You hand over your pot, they pay you a set amount every month until you die.

No investment risk. No worrying about running out. But also no flexibility, once you’ve bought it, that’s it.

You can still take your 25% tax-free before purchasing the annuity.

Option 3: UFPLS (Uncrystallised Funds Pension Lump Sum)

This one has an acronym only an actuary could love. (It’s usually pronounced “uff-plus” if you ever need to say it out loud.)

An UFPLS lets you take lump sums directly from your pension pot. Each withdrawal is split: 25% tax-free, 75% taxable.

It’s different from drawdown because you don’t separate out your tax-free cash first, it’s blended into every withdrawal.

UFPLS can be useful for smaller pots or as a temporary measure while you figure out your long-term plan. But be careful: taking even a single UFPLS triggers the Money Purchase Annual Allowance.

The MPAA: The Trap You Need to Understand

The Money Purchase Annual Allowance is one of those things that catches people out.

Normally, you can contribute up to £60,000 per year into pensions and receive tax relief (or 100% of your earnings, whichever is lower). That’s the Annual Allowance.

But once you flexibly access your pension, meaning you take taxable income from it, your allowance for future defined contribution pension savings drops to just £10,000.

That’s the MPAA.

What Triggers It?

The MPAA kicks in when you:

Take income from flexi-access drawdown

Take an UFPLS (even just one)

Exceed the old capped drawdown limits

Buy a flexible annuity where income can decrease

What Doesn’t Trigger It?

Taking only your 25% tax-free cash (no taxable income)

Buying a standard lifetime annuity

Taking income from a defined benefit pension

Why Does This Matter?

If you’re still working and want to keep contributing to a pension, triggering the MPAA could be expensive. You’d lose out on tax relief on contributions above £10,000.

UFPLS is particularly dangerous here. Because 75% of every UFPLS withdrawal is taxable, taking even a small amount triggers the MPAA. If you want to keep contributing, consider flexi-access drawdown instead, you can take your tax-free cash without touching taxable income.

Once triggered, the MPAA cannot be reversed. It’s permanent.

For more detail on how pension contributions and tax relief work, including the difference between Relief at Source and Net Pay schemes, see our earlier guide: Pension Contributions Explained.

A Quick Note on Tax Relief for Personal Pensions and SIPPs

If you’re paying into a personal pension or SIPP (rather than through your employer), the tax relief works via Relief at Source.

That means you pay in £80, and your provider claims £20 from HMRC, so £100 goes into your pension. Basic-rate tax relief is automatic.

But if you’re a higher-rate or additional-rate taxpayer, you need to claim the extra relief yourself through Self Assessment. Many people forget to do this and miss out on money they’re entitled to.

It’s worth checking.

What If Your 25% Exceeds the Cap?

If you’ve built up a substantial pension, 25% of your pot might be more than the £268,275 Lump Sum Allowance.

In that case, you can still take £268,275 tax-free (assuming you haven’t used any LSA elsewhere). Anything above that gets paid as a Pension Commencement Excess Lump Sum, this gets taxed at your marginal income tax rate.

Alternatively, you could take less tax-free cash upfront and move more into drawdown, spreading the taxable withdrawals across multiple tax years to manage your tax bill.

People with protected allowances may have higher limits available. Check your protection certificates.

Inheritance Tax: The Big Change Coming in April 2027

This is significant. If you’ve been using your pension as an estate planning tool, pay attention.

The Current Rules (Until 5 April 2027)

Right now, most pension death benefits sit outside your estate for Inheritance Tax purposes. Because pension schemes are written under trust and trustees have discretion over payments, the money typically passes to your beneficiaries without IHT.

This has made pensions incredibly useful for passing wealth to the next generation tax-efficiently.

What’s Changing

From 6 April 2027, most unused pension funds and death benefits will be brought into the scope of Inheritance Tax.

Pensions will now count as part of your estate when calculating IHT. Personal representatives will be responsible for reporting and paying any tax due.

The government estimates around 10,500 estates will become liable for IHT when they previously wouldn’t have been, and roughly 38,500 estates will pay more than before.

What’s Still Exempt?

Death-in-service benefits from registered pension schemes remain outside IHT

Spousal exemption still applies. The benefits passing to a surviving spouse or civil partner are exempt

Dependent’s pensions from defined benefit schemes are also excluded

The Double Taxation Concern

Here’s the worry: if you die after 75 and your pension is subject to IHT, your beneficiaries may also pay income tax when they withdraw from the inherited pension.

The government has said mechanisms will be in place to prevent the same funds being taxed twice, but the details are still being finalised.

This is complex territory. If you have significant pension wealth, it’s worth getting advice before April 2027.

What Happens to Your Pension When You Die?

Pensions don’t go into your will. Instead, you nominate beneficiaries using an expression of wishes form with your provider.

Death Before Age 75

If you die before 75, your beneficiaries can usually receive your remaining pension tax-free (subject to some conditions):

Lump sums must be paid within two years of the scheme being notified

They mustn’t exceed the remaining LSDBA

Beneficiaries can also take the pension as drawdown or buy an annuity (both tax-free)

Death at 75 or After

If you die at or after 75, beneficiaries pay income tax at their marginal rate on whatever they receive, whether it’s a lump sum or income from drawdown.

There’s no test against the LSDBA when death occurs at 75 or later.

Keep Your Nominations Updated

Life changes. This could be marriages, divorces, children, deaths. Make sure your expression of wishes reflects who you actually want to benefit. Trustees who look after pension schemes usually follow your wishes, but they need to know what they are.

Why Pensions Are So Tax-Efficient (And When They Might Not Be)

Pensions operate on an EET system: Exempt-Exempt-Taxed.

Contributions are exempt from income tax (you get tax relief)

Growth inside the pension is exempt from capital gains and income tax

Withdrawals are taxed as income

This triple benefit makes pensions one of the most powerful savings vehicles available. For every £80 a basic-rate taxpayer puts in, £100 goes into the pot. Higher-rate taxpayers can reclaim even more.

When Might Pensions Not Make Sense?

You’ve exhausted your Annual Allowance (further contributions face a tax charge)

You’ve triggered the MPAA and can only contribute £10,000

You’re approaching the LSA cap and won’t benefit from more tax-free cash

You’re over 75 and can no longer get tax relief

You need access to funds before the minimum pension age

In these situations, ISAs or other savings might be worth considering alongside (not instead of) pension saving.

Contributing When You’re Not Working

Even if you have no earnings at all, you can still pay into a pension and get tax relief.

The limit is £3,600 gross per year, you pay £2,880, and basic-rate tax relief adds £720.

This works regardless of whether you actually pay income tax. It’s useful for:

Stay-at-home parents

Carers

Anyone on a career break

Children (yes, you can set up a Junior SIPP for a child)

A spouse or family member can make contributions on your behalf too.

Moving Overseas: What Happens to Your Pension?

If you move abroad, your existing UK pension stays put. You can still access it from overseas when you reach minimum pension age.

But the rules around contributions change.

Contributions After You Leave

In the year you leave the UK, you can contribute up to 100% of your UK earnings (or £3,600 if greater) and still get tax relief.

For the next five tax years, you can continue contributing up to £3,600 gross with tax relief, but only to a pension scheme you were already a member of before leaving.

After five years, no more UK tax relief unless you have relevant UK earnings taxed in the UK.

A more detailed article on pensions, ISAs & investments when moving overseas is coming in April.

SIPP vs Personal Pension: What’s the Difference?

A SIPP (Self-Invested Personal Pension) is a type of personal pension. They follow the same tax rules, the same contribution limits, the same access rules.

The difference is investment choice.

Standard Personal Pension

Typically offers a limited range of managed funds chosen by the provider. Good for people who prefer a hands-off approach.

SIPP

Offers a much wider range: individual shares, ETFs, investment trusts, bonds, sometimes commercial property. Good for people who want control over their investments.

More choice means more responsibility. Poor investment decisions can hurt your retirement savings just as much as good ones can help.

For tax purposes, they’re identical.

Using Your Pension to Retire Early

One of the big advantages of private pensions is that you can access them before State Pension age.

Partial Retirement

You could reduce your working hours and use pension income to top up your earnings. This lets you wind down gradually rather than stopping work overnight.

It can also help manage your tax position, spreading withdrawals over multiple years might keep you in a lower tax bracket.

Full Early Retirement

If you stop work entirely before State Pension age, your pension needs to cover everything until the State Pension kicks in. That could be 10+ years.

This requires careful planning:

How much will you spend each year?

What’s a sustainable withdrawal rate?

How long might you live?

What about inflation?

Getting this wrong means running out of money. Getting it right means freedom.

A detailed article on calculating whether you can afford to retire is coming in February.

The Bigger Picture

Pensions aren’t complicated for the sake of it, they’re complicated because they’re trying to balance tax incentives, access restrictions, and death benefits across different types of schemes and changing government priorities.

But understanding the basics of when you can access your money, how tax-free cash works, what triggers the MPAA, and what’s changing with inheritance tax puts you ahead of most people.

You don’t need to become a pension expert. But knowing enough to ask the right questions, and checking that your arrangements are actually working as you expect, is time very well spent.

This article is for general information purposes only and does not constitute regulated financial advice. The value of pensions and investments can fall as well as rise. Tax treatment depends on individual circumstances and may change. Consider seeking independent financial advice before making decisions about your pension.