ISA, JISA, LISA, IFISA and anything else similar

In the earlier piece The ISA Is One of the Best Investment Wrappers… So Use It we explained why ISAs are so powerful. Tax-free growth, tax-free income, tax-free withdrawals, something that is almost unheard of outside the UK.

This piece does something different.

This is the practical breakdown on what each type of ISA is for, who can use them, how they interact, and where people commonly get tripped up (especially with LISAs and IFISAs).

The Three ISA Brackets – ISA, Junior ISA & LISA

All ISAs share a few core rules:

No tax on gains or income inside the wrapper

You can transfer between providers without losing tax protection

Transfers do not count towards your annual allowance if done correctly

The big differences are age limits, access rules, and penalties.

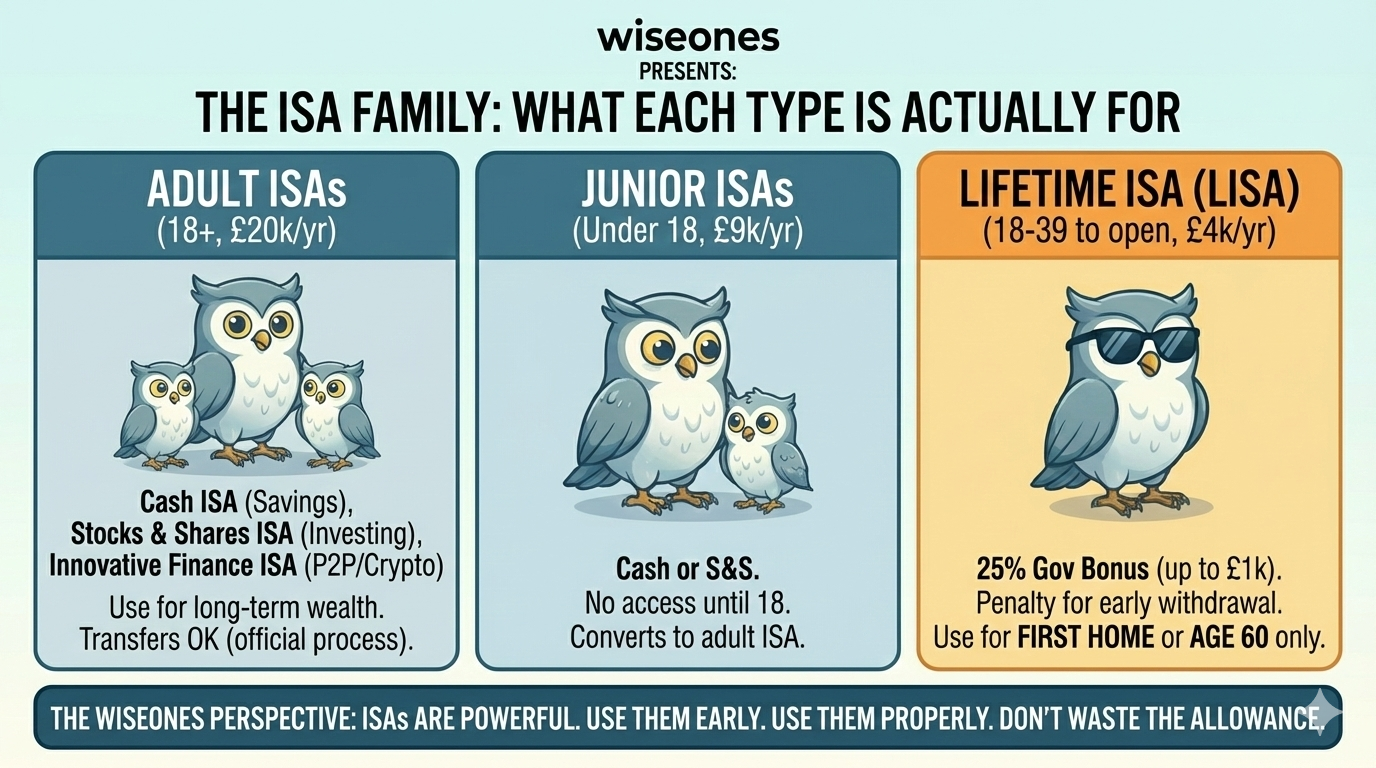

1. Adult ISAs (Aged 18+)

Annual allowance: £20,000

Who: UK residents aged 18 or over

This is the main ISA allowance most people will use. Your £20,000 can be split across:

Cash ISA

Stocks & Shares ISA

Innovative Finance ISA (IFISA)

as long as the total across all adult ISAs stays under £20,000 in the tax year.

Cash ISA

A Cash ISA is simply a tax-free savings account.

It has its place for:

Emergency funds

Short-term spending needs

Money you cannot afford to invest

But as covered in the main ISA article, using a Cash ISA for long-term wealth is usually a poor use of such a valuable wrapper. Inflation quietly does the damage.

If you want to go deep on Cash ISA mechanics, Martin Lewis at MoneySavingExpert has probably forgotten more about them than most of us will ever know.

Stocks & Shares ISA

This is the core long-term wealth builder.

Inside a Stocks & Shares ISA you can:

Buy funds, ETFs, shares, bonds and other assets

Sell, rebalance and switch investments freely

Pay no tax on gains, income or withdrawals

This is where long-term investors quietly do very well. There’s a reason people talk about becoming “ISA millionaires”, it’s not luck, it’s compounding without tax drag.

You generally see two approaches:

Managed ISAs

You choose a risk level or portfolio, the provider does the rest. Ideal for beginners or anyone who doesn’t want to pick investments themselves. Lots of choice and if you don’t know which one, our managed ISA comparison primer will be coming out later this month to help you know what is out there and how they compare.

Again as always we aren’t here to advertise them, no affiliate linking to refer a friend so it will be unbiased in their point of view. A rarity online with finance.

DIY ISAs

You choose everything: funds, ETFs, shares, bonds or a mix. You can blend it to make your own portfolio or there are systematic active investing programs you can use and some places allow you to follow other peoples investment choices and see their past performance.

More flexibility, more responsibility.

Innovative Finance ISA (IFISA)

The least understood ISA, and increasingly relevant.

IFISAs are typically used for:

Peer-to-peer lending

Specialist direct investments

They are not usually offered by mainstream platforms and come with:

Higher risk

Lower liquidity

More complexity

From April 2026, IFISAs become more important because the only way to hold crypto inside an ISA will be via an Innovative Finance ISA.

This is specialist territory. It suits experienced investors with a higher tolerance for risk, definitely not first-timers.

2. Junior ISAs (Under 18)

Annual allowance: £9,000

Who: Children under 18 (opened and managed by an adult)

Junior ISAs can be:

Cash JISAs

Stocks & Shares JISAs

The key rule:

No withdrawals until age 18

At 18, the Junior ISA automatically converts into a standard adult ISA in the child’s name.

From a long-term perspective, a Junior Stocks & Shares ISA is one of the most powerful gifts you can give a child, nearly two decades of tax-free compounding before they even start adult life.

3. Lifetime ISA (LISA)

Annual allowance: £4,000

Who: You must be aged 18–39 to open one

The LISA sits slightly outside the normal ISA rules, and needs extra care. Used correctly, it can be very effective. Used incorrectly, you can get burnt.

What the LISA Does Well

You can contribute up to £4,000 per year

The government adds a 25% bonus

That’s up to £1,000 “free” each year up to the age of 50

A LISA can be held as:

A Cash LISA

A Stocks & Shares LISA

So far, so attractive.

The Restrictions (This Is Where People Go Wrong)

LISA money can only be withdrawn penalty-free for:

Buying a qualifying first home (up to £450,000) or

From age 60

Withdraw for anything else and you pay a 25% penalty on the entire pot — not just the government bonus.

Simple example (cash terms):

You pay in: £4,000

Government adds: £1,000

Total pot: £5,000

If you then need the money:

25% penalty = £1,250

You lose:

The £1,000 government bonus, and

£250 of your own money

This is the bit most people misunderstand.

Why This Gets Worse Over Time

Because the penalty is applied to the whole value, you lose:

The government bonus

Plus part of your own contributions

Plus part of the investment growth

If the LISA is invested and grows over time, the cash amount lost increases, even though the percentage penalty stays the same.

⚠️ Wiseones Warning: You Could Get Back Less Than You Paid In With A LISA⚠️

If you withdraw from a LISA for a non-qualifying reason, you can receive less money back than you personally contributed, even before considering investment risk.

This is one of the very few mainstream investment wrappers where:

The penalty can exceed the government bonus, and

Life changes (job moves, relationships, housing plans) can leave you financially worse off than if you had used a standard Stocks & Shares ISA.

The Wiseones View on LISAs

The LISA is powerful only if you are confident you will use it exactly as intended.

If life goes to plan then great.

If life changes, and it often does, the penalty is unforgiving.

For many people, especially those with uncertain timelines or career mobility, a plain Stocks & Shares ISA can be the safer, more flexible option, even without the government bonus.

Free money is tempting.

Strings attached matter more.

ISA Transfers

ISA transfers are one of the most important (and misunderstood) features.

You can transfer ISAs between providers

You can usually transfer Cash ↔ Stocks & Shares

Transfers do not count towards your annual allowance

But you must use the official ISA transfer process not withdrawing and re-depositing breaks the tax protection.

Special LISA Rule

You can only transfer £4,000 per tax year into a LISA from another ISA

Transferring out of a LISA will trigger the 25% penalties

This makes planning particularly important with LISAs.

Ages & Access

Adult ISA: Open at 18, access anytime

Junior ISA: Open under 18, access at 18

LISA: Open 18–39, access only for first home or at 60

The Wiseones Perspective

If you haven’t already, it’s also worth looking at the flowchart in “Where Do I Start?”, which shows where ISAs sit alongside pensions and other wrappers.

Each ISA has it’s own feature which could be useful, with the most versatile being the Stocks & Shares ISA.

They don’t rely on clever tricks.

They simply remove tax from long-term investing and over time, that’s enormous.

As we’ve shown across the Substack, especially in The ISA Is One of the Best Investment Wrappers… that ISAs are one of the foundations of sensible UK wealth building for everyone.

They’re rare globally.

They’re generous.

And once a tax year is gone, you never get that allowance back.

Use them properly.

Use them early.

And don’t waste them on things they weren’t designed for.