And it really doesn’t need to be overthought

The UK ISA system is quietly exceptional.

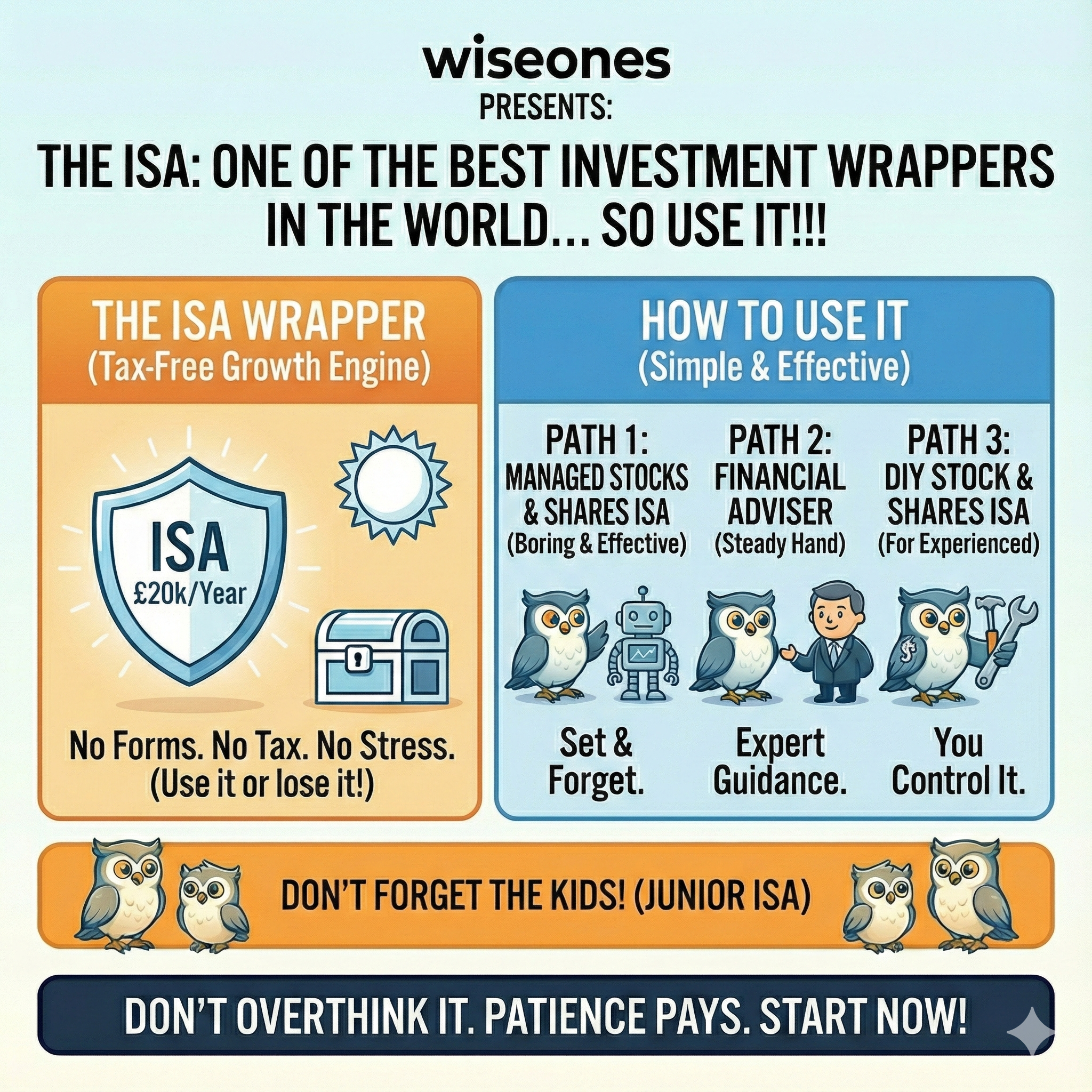

Each year, you’re given an allowance of £20,000 that lets your money grow free from income tax and capital gains tax. No forms. No reporting. No future tax bill waiting in the background. If you’re married then make sure you both make use of the allowance.

Very few countries offer anything like it.

And yet, a large proportion of ISAs sit in cash, often for years doing very little while inflation quietly gets on with its work. We are not here to discus Cash ISAs, there are enough people shilling the best Cash ISAs. We are telling you look at investing not cash.

For long-term money, that isn’t cautious.

It’s costly. Choosing your investments in an ISA doesn’t have to complicated.

An ISA Isn’t an Investment, It’s Just the Wrapper

An ISA doesn’t decide returns.

It doesn’t reduce market risk.

It doesn’t magically grow money.

It simply removes tax.

Inside a Stocks & Shares ISA (and an investment-based Lifetime ISA), you can hold:

Shares and equity funds

Bonds and defensive assets

Multi-asset portfolios

Professionally managed strategies

Once money is inside the wrapper, everything that happens next. The growth, income, rebalancing, it is all tax-free.

That’s the part that makes ISAs special.

Time Horizon Matters More Than Almost Anything Else

Before worrying about what to invest in, the most important question is when you need the money.

A simple guide:

Less than 3 years → cash usually makes sense

More than 3 years → investing should be considered

More than 5 years → keeping everything in cash is likely to mean falling behind

This isn’t about chasing quick returns, the get rich slow method is usually the best.

It’s also about avoiding the slow loss of purchasing power.

How Most People Should Be Using a Stocks & Shares ISA

There are lots of ways to invest through an ISA.

For beginners, there are two sensible routes and both are deliberately boring.

1. A Managed Stocks & Shares ISA

This is where investing becomes refreshingly unglamorous.

A managed ISA:

Spreads your money across different assets

Adjusts risk based on a simple profile

Rebalances automatically

Requires almost no ongoing input

You don’t pick funds.

You don’t watch markets.

You don’t make decisions every time the news gets dramatic.

You answer a few questions, choose a risk level, set up contributions, and let it run.

This isn’t because investing is easy.

It’s because removing decisions removes mistakes.

Honestly, anyone can set up a managed Stocks & Shares ISA and that’s exactly the point.

2. Investing With a Financial Adviser

The other sensible option is working with an adviser.

An adviser adds value not by being clever, but by being steady.

They help:

Match investments to your real tolerance for risk

Keep things aligned with your goals

Stop you reacting at the worst possible time

For many people, that behavioural support matters more than any fund choice ever will.

Don’t Forget the kids!!

There’s also a Junior ISA and it’s one of the most underused long-term planning tools available.

A Junior ISA allows you to invest on behalf of your children up to £9,000 a year with everything growing tax-free until they gain access at 18.

Time does the heavy lifting here.

Investing even modest amounts from birth gives money nearly two decades to compound, something no savings account can replicate.

You don’t need to be clever.

You just need to start.

A simple, Junior Stocks & Shares ISA set up early can quietly become one of the most valuable gifts you ever give your children.

There Are Plenty of Managed Options and We’ll Be Breaking Them Down

One of the advantages of managed ISAs is that there’s a choice of providers.

Different platforms take different approaches to cost and portfolio construction

Some are better than others and not always for the reasons you’d expect.

Over the next few months, we’ll be digging into this properly.

Later in January: a product and performance-led look at the main managed Stocks & Shares ISAs on the market

February: the same analysis for investment-based Lifetime ISAs

March: self-invest ISAs, ahead of the tax year end

The aim isn’t to crown a single “winner”, but to give you enough clarity to choose something suitable before the clock runs down and you lose another year of ISA allowance.

With up to £20,000 available each tax year, the opportunity cost of doing nothing is real.

Why Beginners Shouldn’t Be Building Portfolios Themselves

There’s a misconception that a Stocks & Shares ISA means picking your own investments.

For experienced investors, that can be fine.

For beginners, it’s usually unnecessary and often harmful.

DIY investing assumes you know:

How assets interact

How markets behave in stress

How you’ll react when your portfolio is down 40–60%

Most people only discover their true risk tolerance after it’s been exceeded.

Managed portfolios exist for one simple reason:

they make investing survivable.

The Problem With “Just Buy a Global Fund”

A single global equity fund is often presented as the perfect solution.

Simple. Cheap. Hands-off.

But simplicity on paper doesn’t always translate to simplicity in real life.

Global equity markets fall.

Sometimes sharply.

Sometimes for long periods.

When that happens, investors without structure tend to lose confidence and abandon the plan.

Diversification isn’t about being clever.

It’s about staying invested long enough for investing to actually work.

A Simpler Way to Think About ISAs

You don’t need to be an expert.

You don’t need to follow markets.

You don’t need to pick the “right” fund.

You don’t need a lump sum, just pay in every month.

For most people, a managed Stocks & Shares ISA or an adviser-led solution does the job perfectly well.

ISAs don’t reward cleverness.

They reward patience.

And patience is much easier when the setup is so simple that, frankly, any old idiot can do it and then get on with their life.