A brief guide to pensions, ISAs, VCTs and tax efficiency as we head into 2026

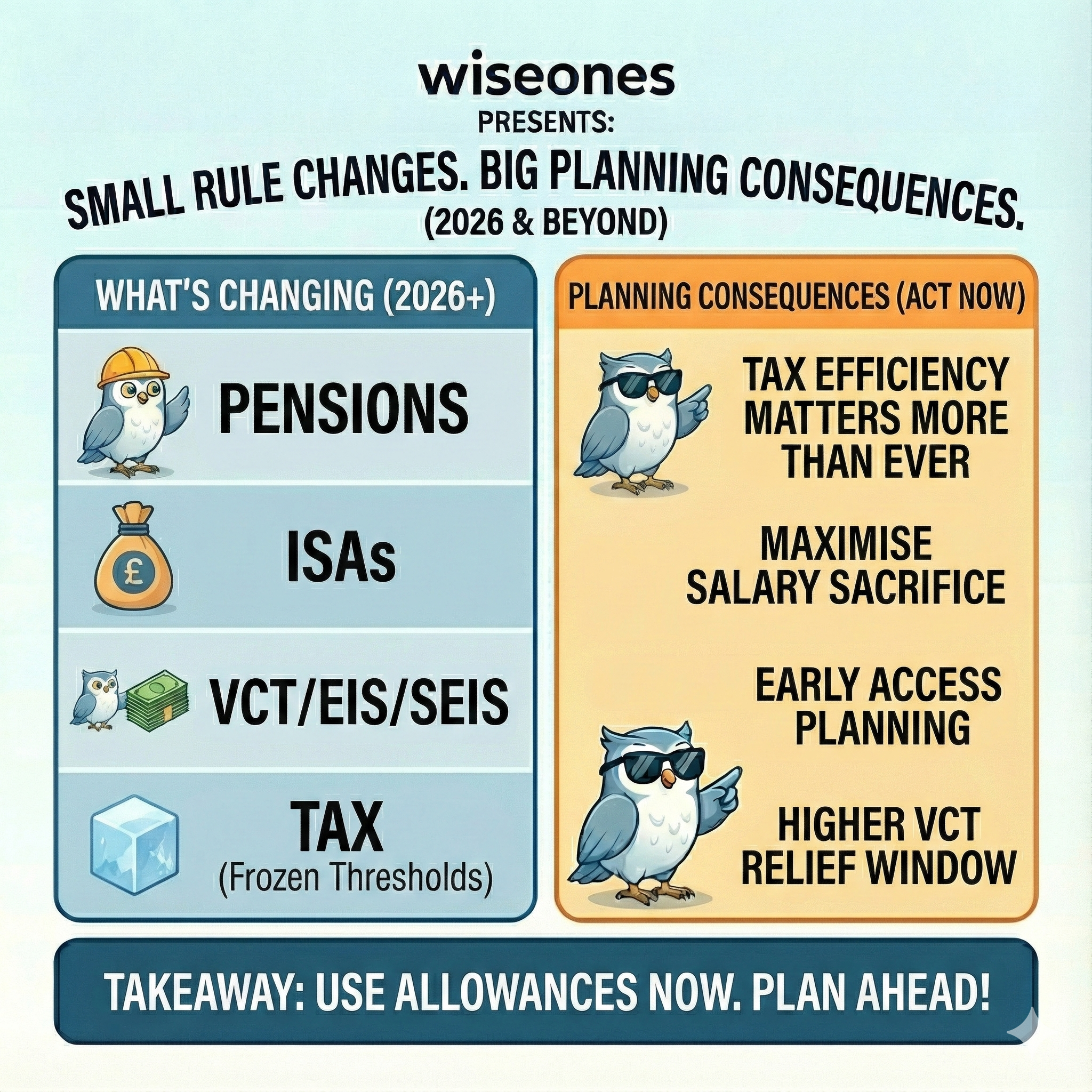

Pensions

✅ £60,000 annual allowance stays.

⏳ Access age rises 55 → 57 in April 2028 : plan early access now if appropriate.

⚠️ Salary sacrifice NI advantage capped from April 2029 (£2k limit) : make the most of it before then.

❓ Pensions & Inheritance Tax still no final rules, but changes expected from 2027 : planning window is now.

⚠️State Pension increases by 4.8% pushing more into paying income tax

ISAs

✅ £20,000 ISA allowance unchanged.

🗣️ ISA reform consultation ongoing – direction of travel is more focus on investing, less cash.

VCT / EIS / SEIS

⚠️ VCT income tax relief drops from 30% → 20% in April 2026 : 2025/26 likely last year at 30%.

✅ EIS (30%) and SEIS (50%) reliefs unchanged – still attractive for higher-risk capital.

Tax

🧊 Income tax thresholds frozen : more people pulled into higher tax.

💡 Tax efficiency matters more than ever.

Takeaway

Use salary sacrifice, pension allowances, and higher VCT relief while they’re still available.

Utilising the £60k pension contributions and going back 3 years besides building up a good pension pot can reduce corporation tax bills.